Money Flow - Part 2

Statistics & Risk Management

Money Flow - Part 2

Statistics & Risk Management

(Note that our discussion of the SOCF uses the indirect method.)

The SOCF is a summary statement showing why the cash account on two adjacent balance sheets changed over the year. It's purpose is to report all activities that produced cash inflow or cash outflow for the year. The relevant questions here are: What activities used cash and what activities produced cash and do adjustments need to be made to these money flows in the interest of better cash flow control?

A further purpose of the SOCF is to clearly identify how inflows and outflows of cash are related to operating activities, investment activities, or financing activities. Given a financial decisionmaker's concern with the ability to track money flows (i.e., cash flows) though the business for a given period of time, being able to explain why the cash account changed (went up or went down) over the year can yield important information in managing these three important categories of business activity.

Additionally such an investigation can lead to other general questions about any apparent developing trends in cash usage or production which could affect the effective functioning of the business in the future. Cash flow trend analysis is critical since if a firm is not "cash flow healthy" then its general health and profitability will ultimately be compromised.

So what's wrong with the income statement as described in Table 2-1 to gauge cash flow health? If the firm is a going concern as described earlier the income statement can be used as a rough approximation of cash flow simply by adding back to net income any non-cash expenses for the year (e.g., depreciation and amortization). However, a non-cash adjusted income statement lacks the precision that decisionmakers need to truly monitor the firm's financial status and cash generating ability.

Why is this the case? Because, as mention earlier, financial statements (in particular the income statement) are constructed according to the accrual method—revenues and expenses are recorded when they are incurred, not when these events produce inflows or outflows of cash. Additionally, many accounts that impact cash flows do not show up on the income statement, but on the yearly balance sheet.

Thus we can think of the process of constructing the SOCF for a given year as a task of "adjusting" the account net income before dividends (EAT from Table 2-1) for what might be termed accrual accounting mis-match. Since accrual accounting matches revenues with expenses in the time period in which they were incurred, a mis-match between the annual recording of revenues and expenses will probably not match the actual inflows and outflows of cash. The SOCF reconciles this mis-match.

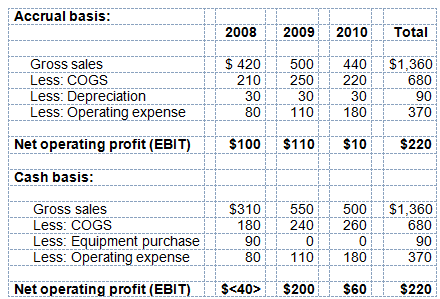

Example: Compute net income on the accrual basis and the cash basis for each year and for all three years in total. The equipment should be depreciated using the straight-line method for the accrual basis over three years. Treat the cost of the equipment as an expense in the period purchased for the cash basis method and assume the operating expenses are paid in cash for both recording methods.

Comment: As you can see the two funds recognition methods produce quite different EBITs; the accrual interpretation of money flows through the firm appears more stable than its cash basis counterpart. This fact could lead to flawed decisionmaking about the operation and stability of the business if the cash basis method is not used in conjunction with the accrual method.

What else should be pointed out about the above table? Let's use 2008 for our discussion. Gross sales in 2008 under the accrual method registers $420 while gross sales under the cash basis method registers $310. Accordingly it must be the case that accounts receivable increased by ($420 - $310) = $110 for year 2008. This fact means that cash was not received for this transaction and constitutes a "use" of funds. An adjustment must be made to net income to reflect this fact. Likewise in the same year COGS under the accrual method was more than COGS under the cash basis method by $30 (= $210 - $180). This means accounts payable increased and was a "source" of funds for the firm. Likewise, an adjustment must be made to the income statement to reflect this spontaneous "loan" and must be recorded on the SOCFs. Finally we see that under the accrual method we "expense" the equipment purchase equally over three years ($90/3 = $30 per year). Since depreciation is a non-cash expense we only see the equipment purchase in year 2008, the year cash when the equipment is paid for. The per year write-off of the asset via depreciation tends to add stability to the accrual report of annual net profit relative to the cash basis method. The transactions for years 2009 and 2010 can be interpreted in a similar manner.

The point is that for many items besides depreciation, changes in accounts receivable and accounts payable can cause recorded net income from the income statement to not equal the firm's cash flow for the year. Thus it is easy to understand that the simple example above will be made more complex as other balance sheet adjustments are incorporated in a formal SOCF financial. The conclusion is that the SOCFs must be considered an integral part of the monitoring of money flows through the firm if financial status is to be kept on track over time.

Constructing the SOCFs for the Zeos Corporation for 2010. We use Tables 2-1 (the income statement) and 2-2 (the balance sheet) to construct the SOCFs for Zeos for 2010. Given that management is concerned with the flow of cash through the firm, it is logical (under the indirect method) to start the construction of the SOCFs by an analysis of the cash account as seen on Zeos' balance sheet. In particular management is concerned why it changed over the years 2009 – 2010. In this context it is best to think of the dollar balance in the cash account at year's end as a residual dollar amount— what's left in cash after all transactions added to and subtracted from the flow of cash over the year. Too many managers simply zero in on the cash balance to judge cash adequacy. This is a mistake.

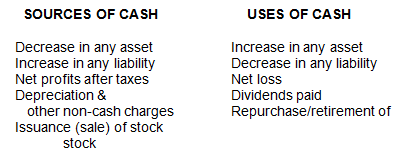

Sources and uses of cash What event categories are sources of cash and what event categories are uses of cash? A brief listing follows:

Note that an increase in the cash account (an asset) is a use of cash; a decrease in the cash account (an asset) is a source of cash. Also note that marketable securities are considered "cash" given their liquidity.

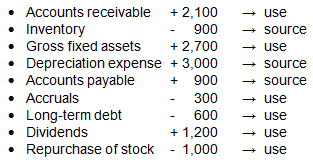

Problem Classify the following account changes as a source or use of cash. A "+" sign signifies a use of cash; a "-" signifies a source of cash. The answers are placed beside the account.

The three net cash flow categories: While the listing of sources and uses of cash is a first step in the construction of the SOCFs, also required is correctly categorizing these net flows. All flow types fit into one of three categories as described below:

1. Net cash flow from operating activities (CFO)—These are cash inflows & outflows that are directly related to the operations of the firm. For example, cash flows resulting from a change in accounts receivable, inventories, accounts payable, or accruals.

2. Net cash flow from investment activities (CFI)—These are cash inflows & outflows that are directly related to the purchase and sale of fixed assets. For example, the cash inflow or outflow resulting from the purchase/sale of new equipment.

3. Net cash flow from financing activities (CFF)—These are cash inflows & outflows directly related to financing the firm's operations. For example, cash flows resulting from a change in notes payable, issuance or repayment of long-term debt, issuance or the retirement of stock, or the payment of dividends.

Because total sources of cash must equal total uses of cash over the year, the following identity results: CFO + CFI + CFF = the change in the cash account (including marketable securities) between two adjacent years. For Zeos Corporation this change is $1.2 million. If this addition does not hold up a math error has been made.

Notice how these categories channel cash sources and uses for the year into three distinct business decisionmaking areas associated with tracing the flows of funds through the business.

Operations is a separate and perhaps the most important category. A general rule is that the business should exhibit cash flow self-sufficient as it relates to its core operations. If Company X makes aircraft engines then its production and sales of aircraft engines (i.e., its "operations") should produce a positive and continuing CFO. Without a healthy CFO over time, the firm cannot continue to exist as a going concern.

The other cash flow categories are important indicators of cash flow health as well. For a growing firm, one that is returning capital back to the firm for future growth, the analyst would expect that CFI activities would be negative. How the firm is financing operations and investments is provided by the yearly net CFF balance. This is a separate cash flow category because it purposely separates the operations of the business from the financing of the business. So doing allows decision makers keener insight into overall cash flow health.

Such questions can then be addressed: "Is the firm issuing debt and then simply recycling the proceeds to prop up lagging operating cash flows?"—a not uncommon occurrence. "Is the firm paying off too much debt so that operating capital might be compromised?" "Are notes payable being used as a permanent source funding for working capital?" "Is the firm paying too much in dividends?"

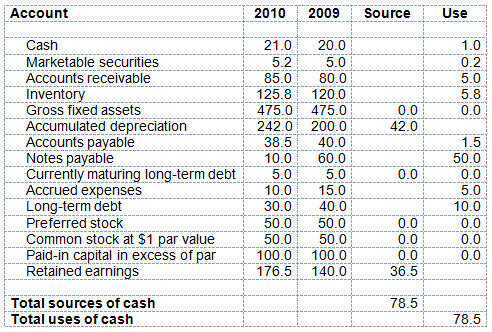

The construction of the SOCF worksheet: If one is unfamiliar with the SOCFs, it is probably best to construct a preliminary cash flow worksheet. It is a matter of simple subtraction of the same account for two adjacent balance sheets. If one is familiar with the SOCF, the preliminary statement is not really needed. We use Zeos' income statement from 2010 and its balance sheets from years 2009 and 2010 from above to do so. Table 3-3A replicates the balance sheet numbers from these two years:

Table 2-3.A. The cash flow worksheet for Zeos, years 2009 – 2010

Comments on the preliminary cash flow worksheet

Notice that total sources and uses of cash equal. This is a good check figure on one's calculations—if they do not equal a transcription or arithmetic mistake has been made.

We see the increase in Accumulated Depreciation is equal to depreciation expense for 2010. Since this expense is non-cash it must be recorded as an implicit source of cash on the worksheet and on the SOFCs. Net income and dividends do not appear on the worksheet since these two amounts are subsumed in the change in retained earnings. While retained earnings is not cash its inclusion on the worksheet is necessary so that the worksheet will balance.

An itemized listing of the steps in the construction of the SOCFs

1. To bridge the gap between the raw financials, the preliminary SOCF worksheet and the and final SOCFs, an itemized listing of steps can be assembled:

2. From the balance sheets of two consecutive years, calculate the change in each asset, liability, and equity account.

3. Classify each change in each account as a "source" or "use" of cash.

4. Obtain net income and depreciation expense for the (last) year from the income statement. If not given on the income statement, obtain dividends from the statement of retained earnings. Classify each as a source or use of cash.

5. Categorize and place all sources/uses into:

a. Net cash flow from operations (CFO)

b. Net cash flow from investing activities (CFI)

c. Net cash flow from financing activities (CFF)

6. Add parts a), b), c) above.This sum should equal the change in cash and marketable securities between balance sheets. If not, you have made a mistake.

It should now be obvious why just a causal recognition of the annual change in the cash account is insufficient to judge cash flow health. As stated above the cash account balance is a residual amount left over after all inflows and outflows of cash have occurred over the year. As a net year-end aggregate dollar amount this number has little meaning for tracking money flows over the year. As the worksheet shows, many items are responsible for the change in the yearly cash balance. Thus management can more clearly monitor funds flow via this preliminary statement. However, ultimately the manager wants to examine the full-blown SOCFs. We compute that below and then use it to provide a complete analysis Zeos' cash flow health in Describing Data module.

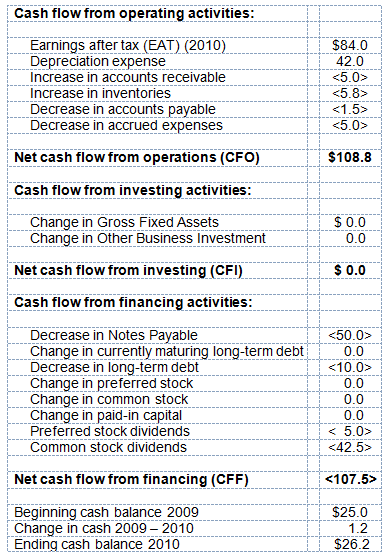

Following along from Table 3-3A we can now assemble the formal SOCFs for the Zeos Corporation for year-end 2010 in Table 2.3.B.

Table 2.3.B. Zeos Corporation Statement of Cash Flows for the year ended December 31, 2010 (in millions of dollars)

Notice that the identity CFO + CFI + CFF = ∆cash and marketable securities from 2009 – 2010 (i.e.,108.8 + 0 + <107.5>) = 26.2 – 25.0 = 1.2.

Important point: In order for management to properly audit cash flows through the firm it is imperative that the correct component accounts appear under their appropriate cash flow category. That is we need to place operating activity cash flows under the CFO category; the investment flows under the CFI category; the financing activity flows under the CFF category. Some incorrect placement examples would be to put dividends in the CFO bucket—dividends have to do with financing not operating the business. Placing investment in plant and equipment in the CFF category would be an incorrect placement—spending on hard assets is not a financing function. An increase in long-term debt would not go in CFO—changes in debt are related to financing, not operating the business. Unlike accounts payable, notes payable, although a current liability, belongs in the CFF category, not the CFO category. This is so since the former is a spontaneous source of short-term credit that will automatically disappear. The latter is a discretionary form of borrowing based upon management's decision to obtain a formally-contracted loan. Hence it is a financing decision and belongs under the CFF category.

Content ©2012. All Rights Reserved.

Date last modified: September 18, 2012.

Created with SoftChalk

mobile page

![]()