The Balance Sheet

The firm's balance sheet shows the firm's assets, liabilities, and owners' equity at one point in time, usually reported at the end of the accounting cycle. It is based on the following accounting identity:

Assets = Liabilities + Owners' Equity

An asset is an economic resource that is expected to produce future cash flows. Assets are either owned or controlled by the firm. A liability is a debtor's claim against the firm's assets. Liabilities are monetary obligations of the firm's stockholders. Owners' equity (or simply equity) represents the stockholders' claims against that part of the assets that are not claimed by the firm's debtors. Equity represents a residual interest in the firm's assets since it is net of the firm's debt obligations. In this context there exists a clear legal distinction between capital supplied by the firm's debtors and that supplied by equity.

Since assets are either owned by equity or claimed by debt, the above equation is an identity, not an equality—it is true by definition.

Thus the dollar value of assets must equal the dollar value of liabilities plus equity. This mathematical fact contained in the identify above in conjunction with the convention of double-entry bookkeeping is typically expressed in a T-account format know as the balance sheet.

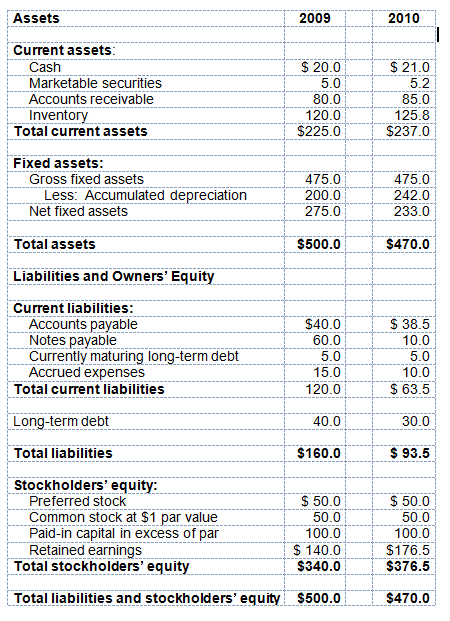

The balance sheet for our hypothetical Zeos Corporation for years ending 2009 and 2010 is shown in Table 1-2 as follows:

Table 2-2 Zeos Corporation: Balance Sheets for years ending December 31, 2009 and 2010

Comments on the balance sheet

The form of a balance sheet's assets, liabilities, and equity accounts shows how the firm's capital structure is assembled, i.e., how much of the firm's assets are supported with debt and how much with equity. Industry characteristics, the type of business (retail, service, manufacturing, information technology, etc.), in conjunction with management's philosophy will help determine a firm's capital structure mix. From the nature of its balance sheet, It appears that Zeos is a conventional manufacturing firm.

Table 2-2 shows that current assets are put first. This indicates the importance of liquidity since these assets comprise the working capital base of the firm. The distinguishing feature of the account called Current Assets is that it contains cash or near-cash (marketable securities) and other short-term assets that are expected to be converted into cash within the year. Accounts receivable represents (credit) sales incurred but not yet converted into cash. This account reflects industry practices and the claims paying practices of the firm's credit customers. Inventory represents items ready for sale or items in the process of being readied for sale (work-in-process). Inventory is listed as an asset but will be converted to an expense item on the income statement account called cost of goods sold when the item(s) is moved out of inventory and sold. Note that inventory valuation methods can be different and that a particular valuation method (LIFO, FIFO, the average cost method) will impact the dollar value of inventory as it appears on the balance sheet as well as the on the COGS account on the income statement. Also note that a re-valuation of inventory (i.e., a mark-down) can occur should the inventory lose value. Mark-downs are attempts by the firm to bring the book value of the inventory into line with its current market value.

Net fixed assets equals the difference between gross fixed assets and accumulated depreciation that has occurred since the assets were acquired. In this sense, depreciation is considered a contra-account since it reduces the historical book value of the asset as a pro-rata yearly amount is written off (accumulated) against the asset(s) over time. So-called impairments and write-downs can be assessed against fixed assets if some sudden event makes a substantial and obvious reduction to their historical book value.

Current liabilities is analogous to current assets in the sense that these short-term debts are expected to be paid within the year. Many firms that manufacture physical products attempt to follow a working capital policy that matches current assets with current liabilities over the year. Accounts payable represent credit sales that come about spontaneously as the firm purchases inventory. It will also disappear spontaneously as the firm pays its vendors. Notes payable, while a current liability, is different from accounts payable in that it is discretionary and results from the firm making a conscious decision to engage in some type of short-term borrowing (perhaps a short-term bank loan or the issuance of commercial paper).

Firms usually issue long-term debt with a maturity structure geared toward paying off the debt issue in yearly increments. In such cases the portion of the debt due in the current year must be considered a current liability. (For Zeros their currently-maturing long-term debt for 2009 was $5 million). This type of debt structure, since it recurs every year, can represent a significant drain on the firm's cash flow position. Accrued expenses represent other short-term liabilities that are due within the year but not yet paid (e.g., wages payable, taxes payable).

Long-term debt represents credit that has a maturity greater than one year. The book value of long-term debt is the summation of all the firm's outstanding long-term bonds at one point in time. It's book value will be reduced yearly as "installments" are made against the debt principle over time.

The equity accounts reflect the legal ownership of the company. As mentioned earlier, preferred stock is considered ownership. However, under financial distress this equity class will (informally if not formally) be reclassified as long-term debt. So preferred stock has a chameleon-like nature. Par value common stock is the firm's nominally-valued equity. The term par value reflects historical precedent and has nothing to do with the price the stock is currently trading for on the market. For example, we saw Zeos' common stock trading at $26.125 at the end of 2009. Also note that the dollar amount of par value can vary and is set by the firm.

The account Paid-in-capital (also know as capital in excess of par) reflects the fact that when the common stock was first issued the stock fetched more than par value per share, in this case for Zeos, twice as much ($100/$50 = 2x). So initial investors actually paid $3 per share, $1 par value and $2 paid in capital. Finally the retained earnings amount of $340 at year's-end 2009 shows the amount of earnings that have been ploughed back into the company since its inception. Understand that retained earnings is not cash, but represents a claim of the common stockholders against the assets on the left-hand-side of the balance sheet. It is a measure of how much the company has "saved" out of earnings since the company began. The retained earnings account will change yearly as net income not paid out as dividends is closed out to retained earnings for the year or as net losses are recorded.

The connection between Zeos' retained earnings accounts at year's-end 2009 and 2010 is shown below. When we combine the retained earnings amounts with the firm's net income and dividend payments in 2010 we get the following results (from Tables 2-1 and 2-2):

In official accounting parlance these calculations are relegated to what's called the Statement of Retained Earnings. This particular statement shows what transactions added to and subtracted from Zeos' retained earned balance between the end of 2009 and the end of 2010. Note that the EAT account adds to net equity while the dividend payments reduces net equity.

This distinction emphasizes the legal separation of the corporation from the stockholder/owners of the corporation. Hence a dividend payment, even though it is paid to the shareholder in an equal dollar amount, reduces the equity of the business by an equal dollar amount. Also note how the cumulative dividends of $47.5 million was determined: The income statement shows that $5 million was paid to preferred stockholders and the remaining $42.5 million (= $0.85 per share x 50 million shares) was paid to the common shareholders.

Managers can use this statement to carry out an ex post analysis of the stability of the firm's earnings accumulation over time. In the above example EAT added to and dividends subtracted from the 2010 ending balance. More generally, a clearer picture of the firm's business stability is enhanced if the ending retained earnings balance grows over time due primarily to the firm's core operations. Excessive mergers, acquisitions, exchange-rate induced currency translations and other activities that can end up on this statement tends to cloud management's perception of the fundamental health of the business at producing core wealth over time.

Digression: The distinction between stocks versus flows in accounting: While the income statement measures flows of dollars over the accounting cycle (say one year), the balance sheet measures the book value of the account items at one point in time (typical at the end of the accounting cycle). Since net income retained in the business is "closed out" to the balance sheet at year's end, a positive (negative) retained earnings will add to (subtract from) the retained earnings account on the balance prior to the beginning of another accounting cycle. Another way of looking at this idea is to consider the assets as the revenue producers (net sales), and the liabilities and equity magnitudes as indicative of how the assets are funded.

Digression: A note on Intangibles and the balance sheet: It is probable that most successful and mature companies areundervalued by their (book valued) balance sheets. We tend to think of the value of a company as mostly embedded in its so-called hard assets—its buildings, machines, and physical equipment. In today's information-based economy, it is probably more accurate to value a company in terms both its hard assets and its intangibles—its human capital, intellectual property, brainpower, its vendor reliability, and its customer base. These items, however, are difficult to monetize and do not appear on the balance sheet. Ironically we have seen the intangible nature of software-producing companies (i.e., brain power) making it difficult for them to raise capital. While this tendency is easing today, in the past banks would much rather have loaned to "hard" brick-and-mortar companies than software producers.