Money Flow - Part 4

Statistics & Risk Management

Money Flow - Part 4

Statistics & Risk Management

1. What is capital budgeting and why is it important?

The overall objective of capital budgeting is to provide management with financial input so that better decisions can be made. In today's business climate, firms either move ahead or fall behind their competitors—there's no "staying even." Growing the business means making financial outlays today so that the firm can move ahead profitably in the future. Capital budgeting is critical to this task and to making good investment choices and avoiding bad ones.

This sounds like a straightforward exercise and in some instances it is. If a storm tears the roof off the firm's warehouse, replacing it would not seem to require all the formality implied by the above definition. So it is probably best to relegate the capital budgeting exercise to major and discretionary investment expenditures that are less than routine in nature. Thus we take a formal view of the capital budgeting process although it can be informal as well. A more formal view of the process will usually relegate the investment task to a special capital budgeting team.

Scarcity and allocation - Scarcity and allocation provide the backdrop for the need to budget (financial) capital. Financial capital is scarce and limited to the firm. Like any scarce resource these funds have a price (called the cost of capital) and must be properly allocated (or budgeted) by the firm. Capital budgeting provides allocation guidance to management so that projects are selected that provide expected returns in excess of their cost.

2. Other reasons accurate capital budgeting is important

3. Motives for capital budgeting expenditures: There are primarily three motives for making major capital expenditures:

(1) Expansion: This motive involves increasing the productive capacity of the firm, usually through the building or acquisition of major fixed assets. The expansion motive is usually geared towards increasing market share via additional sales capacity.

(2) Replacement: This involves replacing existing assets with new or more advanced assets which provide the same function. Replacement is usually associated with an anticipated reduction in the cost of production rather than sales enhancement.

(3) Renewal: This includes rebuilding or overhauling existing assets to improve efficiency. Numbers (2) and (3) can easily be considered part of the replacement process.

Other reasons for making capital expenditures might be for intangibles that are expected to improve profitability. Some examples would be re-educating the workforce, undertaking an advertising campaign, or possibly carrying out government-mandated defensive investment aimed at internalizing negative social costs (e.g, spending on new EPA pollution control equipment).

4. A generic description of capital budgeting as a "process": Capital budgeting is a process in that it follows certain steps that occur over time. Consider this rough outline for an expansion situation.

5. Other important capital budgeting terminology: Capital budgeting comes with its own set of terms and sub-concepts. Let's deal with these here so that we can go directly to the techniques in the next lesson.

Cash flows, not accounting income: Unlike financial statement analysis, capital budgeting deals exclusively with forecasted cash flows, not accrual measures of net income. However, a rough measure of a project's cash flow can be obtained from the accrual-based income statement. An example will be given later in this Lesson Plan.

Investment planning cycle: Project investments are typically not carried out in a random fashion. Rather the firm will usually follow a planning cycle in which a pre-selected number of projects will be undertaken over a given number of years.

Independent versus mutually exclusive projects: A distinction between the following two project types is necessary in order to correctly interpret the capital budgeting directives that will be discussed in Lesson Plan 4B.

Independent projects have cash flows that are independent of each other. Since independent projects perform different functions the firm can undertake as many as it wishes, assuming the firm has the funds and assuming each project meets the requirement that it offers an expected rate of return that exceeds its cost.

Here's an example:

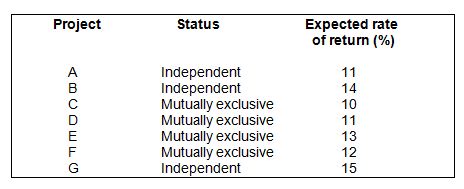

A firm with unlimited funds must evaluate seven projects, A through G, for its upcoming planning cycle. Projects A, B, and G are independent, while C, D, E, and F are mutually exclusive. The seven projects along with their status and expected annual rates of return are listed in the table below. Required: Rank the projects based upon their expected rates of return.

Answer: A ranking of the projects is G, B, E, and A.

Explanation: Since projects C, D, E, and F are mutually exclusive, the highest return of the four, (E) is taken. The others are rejected. All independent projects can be chosen since they do not compete with each other. Note that no decision on which of the four acceptable projects can be made at this time since we do not have information on the firm's cost of capital.

Here's an example:

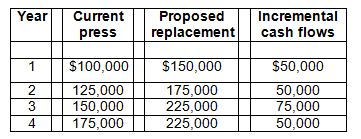

The XYZ Company is considering replacing a current drill press with a new computer-operated model. Both projects have an expected life of four years. The projected levels of net operating cash flows for both presses for the next four years from today are listed below. Objective: List the incremental operating cash flows if the replacement is made.

Example: Firm X is considering expanding its warehouse by adding a second floor and by asking the current tenant that is renting some of the floor space to vacate. Ten years ago the firm built and paid for a railroad spur line leading to the rear of the warehouse. Identify sunk and opportunity costs in this expansion decision.

Answer: The cost of building the second floor is an opportunity cost because the funds could be used elsewhere. The lost rental income that the firm will not be receiving if it asks the current tenant to leave is also an opportunity cost. The spur rail line is a sunk cost and should not be considered in the second-floor expansion decision.

6. Identifying the cash flow categories for capital budgeting: We can identify three relevant cash flow categories for capital budgeting purposes:

(1) the initial investment cash flow

(2) the net operating cash flows

(3) the terminal value cash flow

*Note that the following discussion is still using incremental analysis even if the term "incremental" is not used. A hypothetical set of these three cash flow categories is shown in the following graphic (source, Addison/Wesley Publishing):

Explanation: This graphic displays a conventional cash flow pattern as described above. The initial investment cash flow occurs at time period 0 and is the net amount the firm must spend up-front to get the project started. The operating cash flows are the projected flows that are expected once the project is on-line and producing value for the firm. The terminal value cash flow is the net amount expected to be realized when the project is terminated and sold. In what follows we deal with each category separately. For ease of exposition we will deal with a replacement situation only, one that is has cost reduction (not sales enhancement) effects.

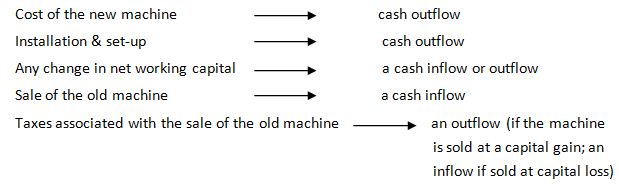

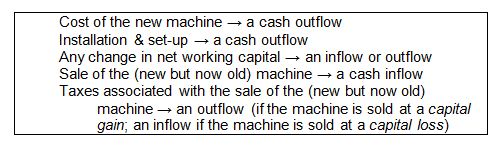

Getting the initial investment (I0): Obtaining the time 0 initial investment concerns more that just determining the raw cost of the new project. In fact, it is comprised of a number of cash inflows and outflows that are ultimately added to give a net cash flow dollar amount. This amount is equal to the initial investment (= I0). A general cash inflow and outflow format follows as it relates to the possible replacement of a current machine with a technologically superior model:

Adding these line-item dollar amounts gives the initial investment = I0.

The first two items are self-explanatory. The replacement may require more net working capital if current assets associated with the replacement exceed required current liabilities. If this is the case then there will be a cash outflow. However, the replacement could result in a smaller amount of related net working capital which would result in a cash inflow since the "old" level of net working capital would be reduced. If the old machine has any after-market value remaining its sale will result in a cash inflow. This inflow must be related to the overall replacement decision, so it's counted here as part of the initial investment.

There may be a capital gain tax on the sale of the old machine if its market value exceeds its book value at the time of sale. This tax would constitute a cash outflow at year's end. Conversely if sale of the old machine is at a price less than its book value the firm can claim a capital loss and use the loss to reduce taxes at year-end. The gain or loss, while either would be recorded at year's end on the firm's consolidated income statement, must be related to the capital budgeting calculations at the time of the analysis. Hence we recognize these calculations at the time of the analysis.

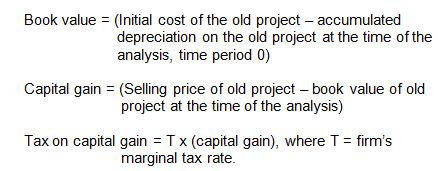

Determining a capital gain or loss on sold equipment: The following equations can help understand the computation of a capital gain or capital loss on the sale of a used piece of machinery.

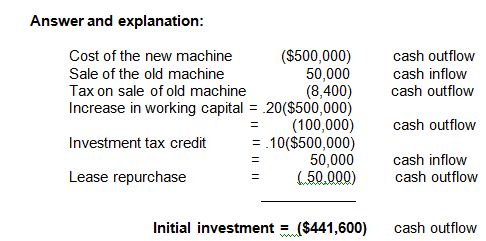

The following represents a comprehensive problem demonstrating how to compute the initial investment with a replacement situation. We add an additional component, an investment tax credit. The credit reduces the net initial investment amount and is allowed by the IRS when the federal government wants to spur new investment by business.

Problem: The Zeos Corporation is considering replacing a current machine with a newer model. The cost of the new model is $500,000. The old machine can be sold in the used market for $50,000. If adopted the new machine will require a one-time increase in net working capital in year 0 equal to 20 percent of the cost of the new machine. If adopted the new machine would allow an investment tax credit of 10 percent of its cost. If adopted the new machine would require the use of a wing of the plant that is currently being rented to another firm. Under the rental agreement the firm can cancel the lease at a cost of $50,000. The current machine initially cost $100,000 and is at the end of the third year of its five-year depreciable life. The machine is being depreciated using the MACRS method. The firm is in the 40 percent marginal tax bracket.

What is the "Initial Investment" (I0) at time period 0?

The only difficult part of this problem is determining the dollar taxes if the replacement is made. Using the above equations we have:

Book value = [$100,000 - (.20 + .32 + .19) x $100,000] = $29,000.

The percentages in parentheses represent the per year MACRS depreciation percentages on a 5-year class life asset. The depreciable base on the current machine is it's historical cost = $100,000. Since the analysis is taking place at the end of the third year of the depreciation schedule for the current machine, we only use years 1, 2, and 3's MACRS depreciation percentages.

So now we have,

Capital gain = ($50,000 - $29,000) = $21,000

Tax on capital gain = .40 x ($21,000) = $8,400

Note the following:

(1) Accumulated depreciation = .71 x $100,000 = $71,000 at the end of year three.

(2) We could have a capital loss if the selling price of the old machine was less than its book value at the time of the analysis. If this were the case the replacement would generate a "tax saving";

(3) While any capital gains or losses would show up on the firm's end-of-year consolidated income statement, for capital budgeting purposes we want to relate the gain or loss specifically to the project involved since the gain or loss bestows an implicit cash outflow or inflow that is related to the project.

Getting the net incremental operating cash flows (OCFs): The net operating cash flows can be thought of as the cash flows generated by the project after the initial investment has been made and after the project is online and up-and-running. Keep in mind that at time 0 no replacement decision has been made; it's still under consideration. So all calculations that follow should be interpreted only in a pro forma manner. It is expected that the net incremental operating cash flows will be positive, although that fact cannot be assumed automatically.

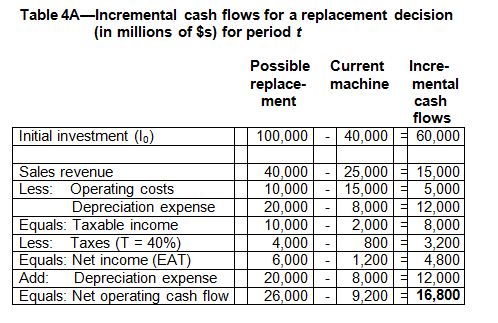

The method of calculation will use the conventional income statement format. If we assume the firm is a going concern, we can ignore any previously discussed accrual mis-match irregularities. This hypothetical example shows that to obtain the net operating cash flows two pro forma income statements for each forecasted period are required, one for the new machine and one for the current machine. This second income statement is assumed to get the cash flows of the current machine if the replacement is not made. All net cash flows are assumed to be forthcoming at year's end. The cash flow for period t both the new and current machines is computed using the following equation:

Cash flow t = [Revenues t - Expenses t] + Depre expense t

Two notes are in order:

(1) We add back depreciation since it's a non-cash expense;

(2) We exclude interest expense from the expenses account since it will be adjusted for in the next lesson using the firm's cost of capital. The first line is displayed for convenience; it is not part of the operating cash flow income statement. It shows the new machine will have a cost of $100,000 and the current machine can be sold for $40,000 net of taxes. This produces an initial investment of $60,000.

Using the conventional income statement methodology we subtract for each account the appropriate revenue and expense accounts for the current "as is" situation from their sister components for the possible replacement. This produces the incremental cash flow column which can be viewed as an incremental income statement for period t . Doing so gives a net incremental operating cash flow for period t equal to $16,800. Note the incremental depreciation amount equal to $12,000. This will provide 0.40 x $12,000 = $4,800 in tax shelter "saving."

Computing the net incremental cash flows in this manner can be a tedious exercise since a typical project can have anywhere from five to ten different forecasting periods (t = 1 . . . 5 . . . ). An added complexity arises if sales and cost forecasts change over the forecasting horizon.

Getting the terminal value cash flow: The terminal value cash flow is the cash flow that results from liquidation of the project at the end of its forecasted life. If the firm follows some type of replacement chain policy where old assets are replaced by new ones, then the terminal value calculation is identical to the calculation of the initial investment. Hence we will not go through a formal numerical calculation here. It is sufficient to repeat the initial investment template again:

Adding these items algebraically will then give the terminal value cash flow.

Comments regarding terminal value: It is quite possible a "no replacement" decision will be made. If this is the case, only the after-tax sale of the (now) old machine would have to be estimated. It is also possible the terminated machine might have been fully depreciated in which case accumulated depreciation would sum to $0. In this case any sale of the terminated machine at a positive price would produce a capital gain and a capital gain tax. It is also possible that the terminated machine might have to be scrapped, a situation that would produce a capital loss tax saving (assuming the machine was not fully depreciated). In this case there would be a recoupment of net working capital (a cash inflow) as accounts receivable would be collected and not continued and as accounts payable ceased to exist.

From a capital budgeting standpoint two important points should be made:

(1) The final cash flow on a projected timeline horizon will consist of two simultaneously-occurring cash flow categories, an operating cash flow and a termination cash flow (if any). This fact is seen in the previously-presented graphic. The two cash flows are simply added to produce a final cash flow.

(2) The termination cash flow can constitute a large percentage of the expected total cash flows associated with the replacement analysis. Hence accurate termination values are important since their value can appreciably impact a capital budgeting decision.

Content ©2012. All Rights Reserved.

Date last modified: October 4, 2012.

Created with SoftChalk

![]()