Money Flow - Part 4

Statistics & Risk Management

Money Flow - Part 4

Statistics & Risk Management

1. A quick review:

In the first part of this lesson, we described the nature of capital budgeting and why it is important for the firm's short-term and longer-term strategic planning. We discussed the distinction between expansion-type projects aimed at increasing sales and replacement-type projects aimed at cost reduction. We emphasized that capital budgeting is fundamentally a forecasting exercise where sales and cost projections are made for a particular project under consideration over some reasonable forecasting horizon. Once obtained, these forecasts can be reduced to three relevant cash flow categories: the initial investment cash flow (I0), the net operating cash flows, and the terminal value cash flow.

Of chief importance in obtaining accurate capital expenditure decisions is the understanding that all cash flow numbers are incremental in the sense that they define the additional cash flow that is expected if a project is undertaken, be it an expansion or replacement situation.

Now we will apply various capital budgeting methods to the relevant incremental cash flows to help cull "good" from "bad" capital budgeting expenditures. A so-called "good" expenditure is one that is expected to add to shareholder wealth. It is these projects that we will invest in. Projects that, ex ante, are expected to decrease shareholder wealth are to be avoided.

3. Some incidental comments:

Why are there so many capital budgeting methods? While we only study three capital budgeting methods in this section, there are, in fact, many methods. One might ask, "If we are using the same cash flows, why do we need so many evaluation methods? Isn't one good enough?"

While this is a fair question we point out that each method sheds a slightly different light on the desirability, or lack thereof, of an investment project's expected profitability or loss and its risk. So to gain insight into these subtle differences it's best to apply as many methods to a given set of cash flow data as possible. With the desktop computer and a multitude of applications software, numerous computations can be quickly carried out with ease.

Don't overlook intuition: The models presented here ultimately come up with an "accept" or "reject" conclusion regarding an investment expenditure. However, keep in mind that this conclusion is based upon a number of assumptions that are assumed correct, (e.g., correct incremental initial investment, operating, and terminal cash flows, a correct forecasting horizon, a correct cost of capital, and a correct assessment of risk, to name a few). However, many factors which will ultimately determine the profitability of an expenditure may not be known or do not lend themselves to a precise incorporation into a strict form mathematical model. The point is that a mathematical accept/reject decision should be viewed as a first approximation only. A final expenditure determination should ultimately incorporate management's past experience regarding the expected project's profitability in addition to what the formal models suggest. Simply put, don't overlook simple intuition in coming to a final accept or reject decision. What's required is a careful blending of mathematical output and intuition in capital expenditure decisionmaking.

Adjusting for risk: The riskiness of the cash flows must be assessed so that an appropriate discount rate can be determined. If a project is of average risk, the firm's weighted average cost of capital (to be described) can be used as the discount rate. If a particular project has above-average risk certain risk-adjustment techniques will be required. A risk-adjusted decision can sometimes differ from its non-risk adjusted counterpart. To ignore this additional capital budgeting complexity is to ignore today's real-world business environment. In this Lesson we will deal with average risk projects only. We will not explicitly adjust for above-average risk in the capital budgeting methods in this Lesson. However, keep in mind that there are numerous risk-adjustment methods which can be employed and which can alter a capital budgeting decision from its non-risk-adjusted counterpart.

"What-if" analysis: What-if analysis should be undertaken so as to assess the expected profitability of the project under different but possible cash flow scenarios.

The idea with this type of analysis is to slightly alter one or more of the equation inputs and recompute the answer. If small but possible alterations to input variables lead to drastically different decision outcomes then management needs to reconsider the initial accept/reject decision. Such simulation analysis is sometimes called stress testing and can reveal how well an investment decision can withstand less-than- favorable economic states that could occur. This is a form of down-side risk analysis in that it emphasizes project outcomes under various possible future states than are worse than expected. For example, if down-side risk analysis shows that an unsuccessful but very costly project might bankrupt the company due to a small alteration of one input, this information should be included in the final spending decision. We will not engage in "what if" analysis here. It is sufficient that you understand what's involved and that stress-testing is quite easy given the application programs that exist for the desktop computer.

4. A common set of cash flows:

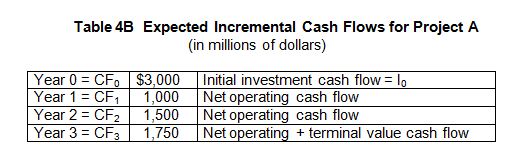

In order to allow meaningful comparison between the three capital budgeting methods we will use a common set of cash flows. These are assumed to apply to Project A and appear in Table 4B below. Remember that cash flows occur at the end of the year. Year 0's cash flow occurs at the beginning of Year 1 or the end of year 0. The cash flow occurring at the end of Year 3 is assumed to include the terminal value.

In the demonstrations that follow these cash flows can apply to either an expansion situation or a replacement situation. If it's the former the initial investment is made up of the cost and installation of the new project, any working capital change requirements, and perhaps an investment tax credit. If it's a replacement situation then we must add any tax consequences (tax on a capital gain or loss) of replacing a current project with a new model. The net operating incremental cash flows are projected revenues less all costs (excluding interest expense) per year over the forecasting horizon (see the Table 4A in previous lesson). The cash flow shown for year 3 is the sum of both year 3's net operating incremental cash flow plus any terminal cash flow occurring at the end of year 3.

Admittedly the three year forecasting horizon for Project A is short; a longer horizon would simply increase the necessary calculations without adding to the overall concepts we are trying to demonstrate. Another simplifying feature is that operating cash flows are assumed to occur at year's end. In real-world situations this would usually not be the case. Using this simplification allows us to skirt tedious intra-year cash flow frequencies and does not change the thrust of the analysis in any meaningful manner. Finally, keep in mind that these are pro forma projections that have been worked up by the capital budgeting team; no decision about the making the expenditure on Project A has been made.

5. The Payback Method (PB)

Note: PB is defined in years plus partial years, not dollars or percentages.

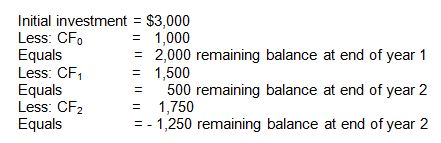

Calculation: Calculation of PB is straightforward and requires only subtraction and long division. For Project A using our projected cash flows from Table 4B we have:

When the remaining balance turns negative after year 2 you know that payback will occur sometime during the year preceding the negative cumulative cash flow. For Project A this is 2 years. However, some of year 2's cash flow is needed to payoff the project during year 3. This amount is computed as the unrecovered cost at the start of year 2 divided by year 3's cash flow, or 500/1,750 = 0.28 years.

Thus the full calculation of Project A's payback is:

PBA = 2 years + 0.28 years (or about 2 years and 3 months).

The formal payback formula is:

And you can see that when the net per year cash flows are equal payback is simply computed as:

![]()

Application: A routine use of payback as it applies to the decision to refinancing a home provides a good example of the method.

When one refinances to take advantage of a lower mortgage interest rate it is necessary to determine the monthly cash flow savings that will occur relative to not refinancing. The fly in the ointment here of course is closing costs which is your initial investment. The other decision variable is how long you plan to stay in the home.

Dividing the dollar amount of closing costs by monthly cash flow savings that will occur due to the lower mortgage rate will give you the number of months (or years) necessary for the cumulative savings to equal the investment in closing costs. If you plan to stay in the home longer than this amount of time you should refinance; if your planned stay is shorter than this time period, you should not refinance.

Example: Mr. Jim can refinance his current mortgage and save $150 per month in installments. He figures his closing costs will be $5,500. He plans to say in the home two years from now before relocating. Should he refinance using the payback method?

Answer: No. His payback on the $5,500 closing cost investment is

5,500/150 = 36.6 months (or 3 years and 15 days). He should not refinance as his monthly cash flow savings does not equal his investment before his planned relocation and sale of the home. Of course, should he plan to stay in the home more than three years, he should refinance.

The decision criteria and payback: The decision criteria for payback is straightforward: When making accept/reject decisions that are independent the following apply:

If we are dealing with a ranking situation where projects are mutually exclusive, pick the project with the lowest PB (assuming it's less than or equal to X years) and reject the others.

Management and "X" years": A unique feature of the payback method is that management must pre-specify the maximum payback period that they are comfortable with (X years). This number of years is subjective and is a function of management's past experience with making capital expenditures and their attitudes regarding expenditure aggressiveness or conservativeness, the type of project (expansion or replacement), its risk, the cash liquidity needs of the company, and many other intangible factors.

Note* the important implication of the subjective nature of setting the maximum payback for stockholder wealth maximization: If management is too aggressive in making capital expenditures X will be too long resulting in a greater probability that projects will be accepted that could compromise shareholder wealth. Conversely if management is too conservative X years will be too short with the result that some profitable projects will not be undertaken thus compromising stockholder wealth.

Payback sum-up: The payback method as a capital budgeting tool is still quite popular even though it is theoretically unsophisticated. Below we list the "goods" and "bads" of the method and leave it at that.

The good aspects of the payback method are as follows:

The bad aspects of the payback method are as follows:

Preliminary material for the Net Present Value and Internal Rate of Return methods—a tutorial:

In order to understand the calculation mechanics associated with the Net Present Value (NPV) and Internal Rate of Return (IRR) methods some initial concepts need to be described. The first has to do with Present Value, discounting, and opportunity cost. The other has to do with the firm's Weight Average Cost of Capital (WACC). Without a cursory working knowledge of these concepts the NPV and IRR calculations and their ability to cull good from bad projects will not have much meaning. So consider the following a tutorial. If you have already seen these ideas in other courses you can proceed directly to section 6B.

Note: When you work NPV and IRR problems you are solving one equation in one unknown—like you did in your high school algebra course.

Present value: Present value (PV) is defined as the dollar value today of discounted cash flows expected to be received in the future. Present value is one specific aspect of the more general topic called Time Value of Money. We are concerned with present value since both NPV and IRR are computed using cash flows expected to be received in the future.

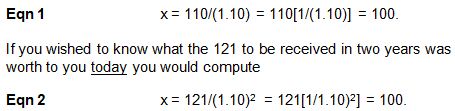

Example: If you invest $100 today at 10% for one year at year's end you will have $110. That is 100 + .10 x100 = 100(1.10) = 110. The term (1.10) is equal to the appreciation factor for one year at 10%. It shows how much your initial investment of 100 will grow over the year. If you rollover the 110 at the end of year 1 again at 10%, at the end of year two you will have 110(1.10) = 100(1.10)2 = 121. The exponent takes care of compounding or interest-on-interest and is the appreciation factor for two years at 10%. We could continue this example, but it's not necessary to do so.

Now, if at the end of year 1 you wanted to know what your 110 (to be received at the end of year 1) was worth to you today, you would take the above equation

100(1.10) = 110

and solve it for 100. That is:

In the above two exercises we computed the present value of a lump sum to be received in the future.

Using a little algebra we can express the denominators as [1/(1.10)] and [1/(1.10)2]. These are known as discount factors. They are equal to 0.909 and 0.826, respectively in that they reduce the dollar value of the amount to be received in the future. This reduction reflects the opportunity loss you implicitly suffer by having to wait one and two years, respectively, to get your hands on the cash. Notice how the discount factors decrease in value as the time to receipt of the cash flow increases.

A digression on PVIF factors: These denominators are also call Present Value Interest Factors (PVIFs for short). A PVIF is defined for a given interest rate and number of years. For example the PVIFs in the above two-year example would be for year 1:

(PVIF10,1) = [1/(1.10)] = 0.909 , and for year 2 it would be

(PVIF10,2) = [1/(1.10)2] = 0.826.

The first subscript indicates the interest rate; the second subscript indicates the time period. So we could write Eqns. 1 and 2 as follows:

As you can see the PVIF factors are simply a convenient way to skip all the math. However, keep in mind that they are quite limited since you still need to use your calculator (or Excel) if your interest rates or time periods are not a full integers.

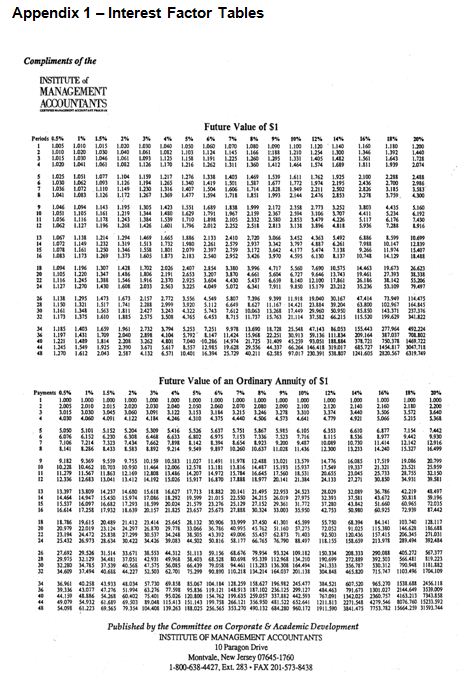

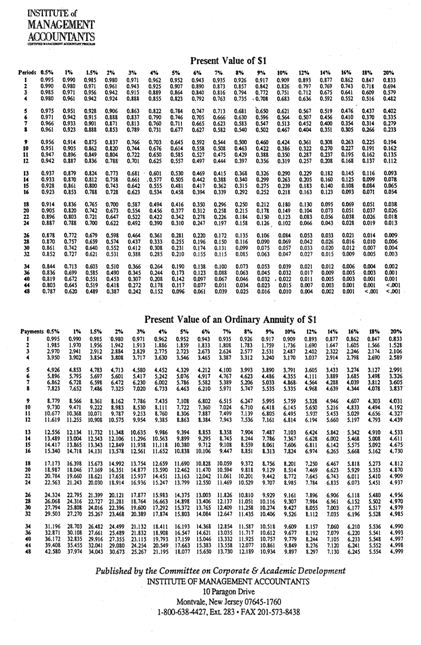

Appendix 1 shows a PVIF table (make sure you are looking at the PVIF and not the PVIFA portion of the appendix). This table gives numerous PVIF interest factors where the general notation is (PVIFk,n). The interest rate is given across the top row and the time period is indicated in the vertical column on the left. The interest factors will be displayed in the appropriate coordinates. Check out Appendix 1 and make sure you can locate our two discount factors.

Back to discounting: Note that without discounting the absolute dollar values are not comparable because they are received at different points in time in the future. You cannot add 110 + 121 = 231 and interpret the 231 as a present value due to the fact that the two amounts are not in comparable units in terms of time to receipt. They can only be added if they are comparable magnitudes and discounting produces this comparability. So if you were going to receive cash flows of 110 at the end of year 1 and 121 at the end of year 2 and the interest rate is 10%, then you could compute the sum

x = 110/(1.10) + 121/(1.10)2 = 100 + 100 = 200.

This sum is known as the present value today (PV0) of 110 and 121 to be received at the end of years 1 and 2, respectively if the interest rate = 10%.

The general PV equation for an n-period horizon is:

![]()

CFi = the expected cash flow occurring at the end of year i, N = the number of years in the forecasting horizon, and k = the discount rate. For our purposes this discount rate is called the weighted average cost of capital (WACC). While it replaces the interest rate term in the above examples it acts just like the interest rate in terms of the math. We discuss the WACC in the next section. Notice from Eqn. 2 that PV is directly related to higher expected CFs , is negatively related to higher N values, and is inversely related to higher k values.

It is important to note the following:

![]()

Obviously it may be difficult to come up with an exact PV due to the uncertainties associated with the expected cash flows, the length of the time horizon, and the correct discount rate. Nonetheless, the above statement is still true and one you should remember since it has important implications for both NPV and IRR.

Summing up so far: So how does all this relate to NPV and IRR? Capital budgeting expenditure decisions are made today, not in the future and are based upon expected future cash flows properly discounted. In order to make correct decisions, management must have some idea of the investment expenditure's value today so that comparisons (and decisions) can be made today. It's that simple.

The weighted average cost of capital (WACC)

In order to employ and then make capital expenditure decisions using NPV and IRR we need a discount rate like you see in Eqn 3. That discount rate is called the firm's weighted average cost of capital (or WACC for short). In Eqns 1 and 2 above the discount rate was 10%. If you had loaned money to the firm with the promise of receiving $110 in one year and $121 in two year's, this 10% would be your required rate of return. From the firm's perspective this same 10% (adjusted for taxes) would be their WACC—they must pay you your required rate of return or else you won't lend them money. Hence the 10% is their before-tax cost of capital.

Numerous sources of capital: Well firms obtain capital from numerous sources. The three main sources are debt capital, preferred stock capital, and equity capital. Each has a different cost (i.e., a different required rate of return). So in order to get the firm's overall cost of capital it is logical to calculate an average cost. Since the three sources of capital are raised in different proportions depending upon the firm's capital structure, we must compute a weighted cost or the WACC.

Example: Firm Z obtains debt capital at an after-tax cost 5.6 percent, preferred stock capital at 10.6 percent, and equity capital at 13.0 percent. These sources are raised in the following proportions (or weights): debt—40%, preferred stock—10%, and equity—50%. (Notice how the percentages sum to 100). Multiplying (or weighting) the costs by their appropriate weights we get the WACC for Firm Z as follows:

WACC = 0.40 x 0.056 + 0.10 x 0.106 + 0.50 x 0.130 = 0.098 or 9.8%.

This is the firm's WACC and is the appropriate discount rate seen in Eqn 3 for NPV and IRR calculations. Why is it the appropriate discount rate? Answer: Because the 9.8% represents the average risk-adjusted opportunity rate for the firm's investors using Firm Z's particular capital structure. They must earn this rate on average lest they will not provide Firm Z with financial capital.

The hurdle rate: Also note that the WACC can be interpreted as the firm's hurdle rate in that the expected rate of return on any capital expenditure must exceed this rate in order to provide shareholders an expected increase in wealth. It is the minimum rate investment projects must provide to be acceptable. For our Firm Z ,"renting" capital at a 9.8% rate and then investing it in projects providing an expected return exceeding this hurdle rate provides a return sufficient to cover the WACC and then some. The additional expected return over the WACC is where the motivation comes from in undertaking profitable investment projects. In effect, NPV and IRR isolate this additional return in order to determine an accept or reject decision.

Defining and calculating Net Present Value (NPV)

Mathematically we can write NPV as:

![]()

where k = the WACC and CF0 = the initial investment, I0, and is negative in value as previously defined in Lesson Plan 4A. FromEqn 3 you can see that the term in brackets equals the PV0 of the discounted cash flows. The NPV equation can be more compactly written as:

![]()

Thus a project's NPV is exactly what it says—the present value of the cash flows net of the initial investment cost. And note that NPV is denominated in dollars, not percentage rates of return.

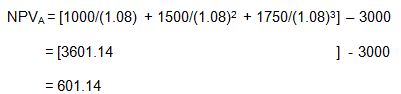

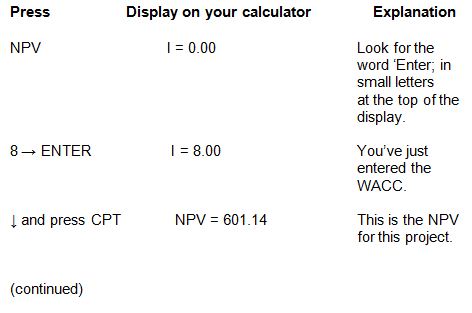

Application: Let's apply the cash flows from Table 4B to compute the NPV for Project A. We will assume a WACC = 8%.

Note: The initial investment, 3000, is in fact discounted at 8%, i.e., 3000/(1.08)0 = 3000/1.00 = 3000.

From what we have said above you can see that the present value of the cash flows discounted at the WACC equals $3,601.13.

With equal generality this NPV could be obtained using PVIF factors as seen in Appendix 1. In this case the equation would be written as follows:

Using your calculator: Any business calculator will have a pre-programmed NPV function on the key pad. Obviously it is much easier to do the calculations via a calculator than by grinding out the numbers above. We went through the "by hand" method simply to make sure you understand what you are doing and so that you will not be mislead by the correct button-pushing necessary to make the calculator display the correct answer. In Appendix 2 we give the steps to obtain NPV on the Texas Instruments BAII+. Other calculators have different data entry methods but they all basically do the same thing. With the TI the only possible pitfall is entering the appropriate cash flows in the cash flow registry entry button entitled "CF." The calculator steps are outlined for this problem in Appendix 2. You should try the instructions in Appendix 2 to make sure you can work your calculator for any set of cash flows and any WACC. Of course if you don't want to use your calculator you can always resort to the PVIF factors.

Rationale and meaning: Now that we have computed the NPV for Project A, what does it mean? How do we use this dollar amount as a rationale for accepting or rejecting Project A?

There are two ways to answer these questions:

1. A positive NPV for a project means that the project is expected to add to shareholder wealth. It is a monetary value reflecting the monopoly position embedded in the project and that was discussed in Lesson Plan 4A.

Note that this an expected amount today, not at some point in the future. That is the NPV calculation results in an ex ante number and is reflected in an immediate increase in expected firm value if the project is undertaken. In this case that amount is $601.14. Subsequently of course, the value increase may not occur. However, investment decisions must be undertaken today and are based upon the immediate expectation that they will increase value. For example, we often see a firm's stock price quickly rise upon the announcement that the firm will undertake a new capital spending program—before a penny has been spent. The rise in stock price is reflecting the immediate increase in expected wealth that is anticipated to accrue to the stockholder. Hence the stockholder (and the market) is willing to pay more for the stock than before the announced capital expenditure.

2. A positive NPV is evidence that the expected rate of return on the project exceeds the firm's WACC. That is, the expected rate of return equals the cost of capital necessary to purchase the project and then add some amount over this hurdle rate. We will see how much extra return is expected when we discuss Project A's internal rate of return. As we will see, if a project's NPV just equals $0, then it only offers an expected rate of return equal to the cost of capital and the project is not expected to increase shareholder wealth.

The decision criteria and NPV

Independent projects:

Mutually exclusive projects:

Conclusion for Project A: If Project A is an independent project it would be accepted. If Project A is one of a list of mutually exclusive projects its acceptance or rejection would depend upon whether or not it ranks at the top of the list. If it does choose A and reject the others.

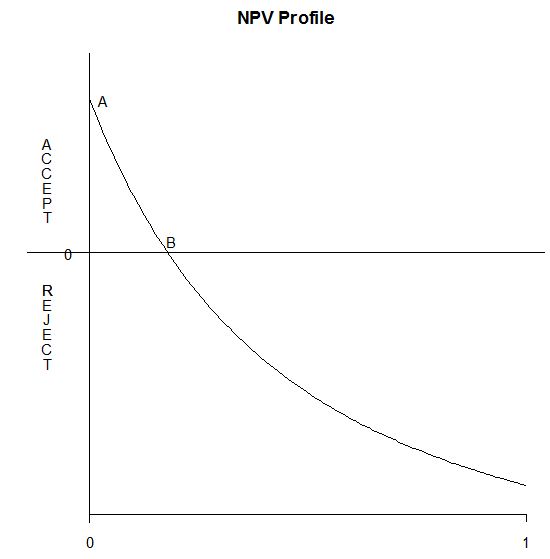

The NPV Profile Graph: A very useful graphic in studying NPV (and IRR) is the NPV profile. The profile graphs the NPV function as a general form, NPV = f(CFs, k, n). Looking at the specific form given in Eqn 4 above we see the profile graphs NPV against various values of the discount rate, k, holding all other variables in the equation constant.The graphic appears below in Figure 4B-1. (Sorry I didn't have graph paper so this is drawn by hand and looks pretty sloppy):

A couple of things to note about this graphic: The relationship between (the dependent variable) NPV and the discount rate is inverse. Since the function is based upon a 3rd degree polynomial equation (in this case) the function is not a straight line. The vertical intercept (point A) occurs when the discount rate equals zero. In this case the intercept is simply equal to the sum of the non-discounted values seen in Eqn 4. Points above (below) NPV = 0 on the vertical axis indicate the acceptance (rejection) regions of the function. When the function crosses the horizontal axis (point B) the NPV = 0. We will return to this feature of the profile later.

Slope and position of the NPV profile: The position and slope of an NPV profile are determined by four variables, the initial investment amount, I0, the size of the cash flows, the timing of the cash flows, and the total number of cash flows. The slope is particularly sensitive to both the timing and size of the cash flows. In terms of timing, a steeper-sloped function will be produced when most of a project's cash flows come due later in its life. In this case these far-off cash flows are discounted very heavily thereby producing a marked decrease in the NPV value for a given change in the discount rate. In terms of cash flow magnitude, a steeper-sloped function will be produced when the cash flows are relatively small over the life of the project. The position and slope of any NPV profile will depend upon the collective interaction of the terms in the general function, NPV = f(CFs, k, n). We could be more specific about the slope and position of an NPV profile but let's not get into these messy details here.

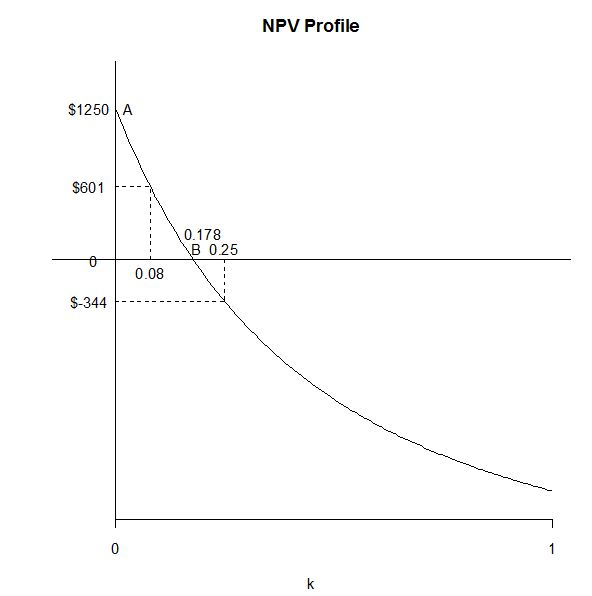

Application: Applying the NPV profile to Project A's discounted cash flows we have the following graphic 4B-2:

We seen that when the discount rate equals the WACC of 8% we get the NPV for Project A as computed earlier ($601.14) using Eqn 5. The vertical intercept is given as $1,250 and occurs when the WACC = 0 in Equation 5. However, the function slopes downward at higher discount rates greater than 0%. One particularly important discount rate is 8% = WACC. Here the NPV function produces an NPV of $601.14. If we continue increasing the discount rate out to 17.81% we get the horizontal axis intercept where NPV = 0. Note that an NPV of $601.14 is in the accept region of the graphic. Also note that discount rates greater than 17.81% produce negative NPVs. For example, at a discount rate of 25% the NPV = -$344.00 (try it). How did this happen? Well the cost of capital was so high that the expected cash flows do not recoup the cost of the funds necessary to undertake the project.

So is the horizontal axis referring to discount rates or WACCs? Both in fact. A particular discount rate that is designated as a WACC will produce its unique NPV and will lead to either an accept or reject decision.

Conclude: Using NPV as your decision criterion we can conclude that Project A should be accepted since $601.14 > $0.

6C: Defining and calculating the Internal Rate of Return (IRR):

There are two conventional definitions of a project's IRR:

The second definition is:

Using either Eqns 4 or 5 you can easily see that a project's IRR is a plug number. That is Defn 1 is a mathematical truism. As such it's not really a definition at all. Thus Defn 2 is the more appropriate way to describe what IRR means.

Caution about the IRR: There are two important cautions about what a project's IRR really represents:

(1) the IRR is not the market interest rate;

(2) the IRR is not the WACC—the IRR and WACC are independent;

(3) the IRR is computed assuming the absence of any financing costs (i.e., the cost of capital).

Thus, an IRR is really the intrinsic rate of return of a project since it's based purely on projected cash flows excluding any costs the firm must pay to obtain or retain the financial capital necessary to make the initial investment, I0. However, the projected cash flows upon which the IRR is constructed do contain other types of costs seen on a pro-forma income statement such as COGS, general operating expenses, and taxes, but these income statement-derived cash flows exclude interest expense.

Computing IRR While Defn 1 is a truism it's still useful in computing IRR. Consider part of Eqn 4 repeated here for convenience:

![]()

Replacing CF0 with - I0 and re-writing the equation with I0 on the left side of the equal sign we have

![]()

Now following along from Defn. 1, to find a project's IRR one must search for a k value such that the dollar amount of the initial investment just equals the present value of the cash flows. Once you have this particular k value, you have the project's IRR. Well this task could leave you searching all day! It's much easier to let your calculator do the walking. Excel is just as good, but let's stick with your TI calculator.

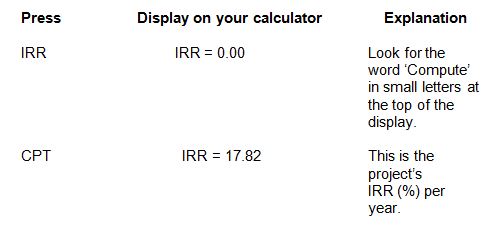

Appendix 2 again: Part 2 of Appendix 2 shows you what to do. You need to work through this appendix with calculator in hand. Notice that you enter the cash flows in the same way as you did when you computed the NPV. After you've done that go to Part 2 of the appendix and follow the directions. You will get 17.82% in your display. This is Project A's internal rate of return. It's the plug number that renders the left-hand side of Eqn 6 equal to the right-hand side of Eqn 6. Using Defn. 2 it's also the expected annual rate of return on the project assuming the project's cash flows are re-invested over the life of the project at a rate of return equal to 17.81%.

Appendix 2

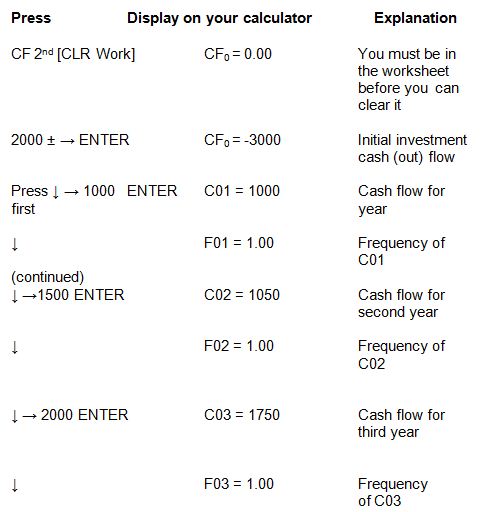

Entering cash flows for NPV and IRR analysis in your TI-BA2+ calculator

(Before you begin make sure the "F" values show 1.00 in the display. You can check this by first pressing the 2nd button. Then press the P/I button. You should see F0 = 1.00 in the display. If not, enter 1.00 and hit the Enter button.)

Example :Assume a project costs $2000 (This is the "initial investment). It is expected to produce the following net cash flows for the following three years and then be disbanded with a salvage value = $0. The WACC = 8%.

Year 0 <3000>

Year 1 1000

Year 2 1500

Year 3 1750

Entering the cash flows into your calculator. This is the same for either NPV or IRR:

Now, all cash flows for are entered. Use them for either NPV or IRR.

1. To get the NPV for Project A:

2. To get the IRR for this project you enter the cash flows in an identical fashion as described above. Then:

What's this reinvestment rate assumption all about? Well the mathematics of the IRR calculation require this assumption. Using Project A's expected operating cash flows that means that year 1's $1,000 will be reinvested for two years in new projects yielding 17.81%; year 2's expected operating cash flow of $1,500 will be reinvested for one year at 17.81%; year 3's expected cash flow of $1,750 will not be reinvested (but simply claimed) since the end of year 3 is the also the end of the project's forecast horizon.

You might question this reinvestment rate assumption. If you did you would be justified in doing so. More on this assumption later.

The decision criteria and IRR

Independent projects:

Mutually exclusive projects:

Rationale and meaning: A project's IRR is a "pure" rate of return in that it is the return obtained from an investment expenditure when that expenditure is made as if the funds needed to make the initial investment were free. Well financial capital is not free. So what's the rationale that can lead to the above decision criteria?

What IRR does is compute a rate of return based upon expected net cash flows where those cash flows reflect all the conventional revenue and expense items seen on the pro forma income statements over the forecasted life of the project (see Table 4A in Lesson Plan 4A for an example) excluding any financing costs that might be associated with the project expenditure (usually this would be interest expense since interest expense is what shows up on an income statement). Then, once the "pure" IRR is obtained the financing costs reflected in the WACC are brought to the front burner for comparison. Since both the IRR and WACC are stated in annual percentage terms they are comparable. These comparisons can then lead to the accept/reject or rank order decisions listed above.

It's that simple and that intuitive: If a project offers an IRR that exceeds the WACC, then that project should be accepted. Using our Project A we see that A should be accepted since IRRA > WACC. In particular we see that Project A offers an expected percentage "profit margin = 17.81% - 8.00% = 9.81%. In effect the firm can "rent" capital for 8 percent per year and put that capital to work for 17.81 percent. The 9.81% spread represents the expected increase in shareholder wealth by undertaking Project A and is the spread produced by the monopoly position embedded Project A.

The relationship between NPV and IRR There exists an exact relationship between NPV and IRR. Verbally this relationship is as follows:

In algebra terms let's re-state Eqn 5:

![]()

Now, let's restate our first definition (truism) of IRR:

Restating Defn1 in equation form where the cash flows have been discounted by the IRR we have:

![]()

Now since I0 = PV0 we can write:

![]()

But this latter expression is the right-hand side of Eqn 5. Substituting the expression into Eqn 5 we have:

![]()

Conclusion: When a project's NPV = 0 the discount rate of the project equals its IRR. This proof is seen graphically in Figure 4B-2 above. Specifically for Project A when it's NPV = 0, we have the NPV profile function crossing the horizontal axis at the project's IRR of 17.81%.

Summarizing: In general we can say the following regarding NPV and IRR for a given project:

You might wonder why a project should be accepted with an NPV = 0 and an IRR = WACC. Remember, investors require at the minimum the WACC on a project. An NPV = 0 situation provides this minimum rate of return. In real-world practice however, a decision made about a zero NPV project would probably be made on additional considerations besides NPV and/or IRR. For example, a decision to go with a zero NPV project (IRR = WACC) might be made with the expectation that the project, undertaken today, will allow the firm the option to take advantage of a possible fortuitous turn in the market in the future. This real option would then give the conventionally-compute NPV using Eqn 5 some additional value not captured by Eqn 5. Other examples like this could be provided but they get into the complexities of real options in capital budgeting. This side topic is beyond the scope of our Lesson Plan.

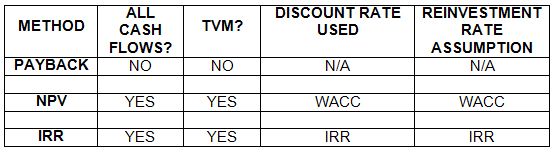

6D: Would the "best" capital budgeting method please stand up!

We have looked at three capital budgeting methods, payback, NPV, and IRR. Are there traits associated with the three methods which can render one method superior to another? The answer is "Yes."

Below is provided a convenient rubric to judge the three capital budgeting methods we have covered. The rubric is based upon four criteria:

(1) does the method consider all forecasted cash flows;

(2) does the method use time value of money;

(3) what discount rate does the method use;

(4) what reinvestment rate assumption does the method make.

While regular payback is a popular method (because it's easy to understand), theoretically it is a no-show since it meets none of the accepted capital budgeting requirements. It would seem that both NPV and IRR are equal in theoretical acceptability; both methods consider all forecasted cash flows, and both use time value of money methods. The only difference is the discount rate used and the reinvestment rate assumptions imposed.

The reinvestment rate assumption used by NPV and IRR: It's the reinvestment rate assumption, primarily, which makes the NPV method superior to IRR. Recall that since that IRR is a plug number it automatically (i.e., mathematically) imposes the assumption that cash flows will be reinvested at the computed (plugged) IRR percentage.

So what's wrong with this assumption? The assumption may not hold, especially for projects that are potential blockbusters and therefore produce inordinately high cash flows and IRRs. Blockbuster projects can be few and far between, but without them the firm cannot reinvest the generated cash flows of the expected blockbuster project so as to produce the plugged IRRBLOCKBUSTER. If the assumption does in fact hold over the life of the project, then the project will earn the computed IRR. However, if it doesn't—if the reinvestment rate assumption falls apart and a project's cash flows cannot be reinvested in new projects that earn the high IRR, the ex post IRR will not equal the ex ante (promised) IRR. Result: The firm may invest in a project that turns out to be less profitable than expected or even a loser.

Realism and plugged IRRs—some examples: Is it realistic to believe a project's IRR might not be accurate due to a bogus reinvestment rate after the project begins to generate cash flows? Absolutely . Many new blockbuster projects typically produce IRRs that are simply too high to be sustainable.

Some quick examples are the advent of the glass-lined water heater after WWII. Prior to glass-lined water heaters the water tank would rust within six months requiring the heater to be replaced. In 1946 Maytag brought to market the glass-lined water heater. Glass does not rust and the new heaters lasted much longer and were an immediate hit with the public. In 1982 the Lotus Development Corporation brought to the software market the original Lotus spreadsheet. Next to the wheel, the Big Mac, and Peronni, the electronic spreadsheet is quite an invention. It was an immediate blockbuster for the company. In 1996 Pfizer brought to market Viagra. For reasons I will not go into in mixed company the little blue pill became an instant success. (Watch out guys, I've heard it causes blindness!)

If someone would have carried out IRR analysis on these projects prior to their development (assuming the sales, cost, and cash flow forecasts were accurate at the time of development), the IRRs of these projects would have been astronomically high—surely higher than the cost of capital. But remember, the accuracy of these computed IRRs would have been contingent upon the ability of Maytag, Lotus Development Corporation, and Pfizer to reinvest the projected cash flows into new projects with equal high rates of return.

Clearly the reinvestment rate assumption was a false assumption in these three cases: Through slight design changes other water heater manufacturers were able to mimic the glass-lined water heater, thus skirting Maytag's patent. Additionally Maytag simply could not find such great (new) projects in which to reinvest the cash flows of the glass-lined heater at its initial IRR. The electronic spreadsheet was soon copied (in slightly different formats) by everyone and his mother-in-law. This competition drastically reduced the projected cash flows to the company. As we know from the flood of (somewhat obnoxious) television commercials, many other pharmaceutical companies have come out with there own version of the little blue pill. (By "version" I mean mild alterations in the molecular structure of the pill so as to just skirt the patent laws—them lawyers and chemists are smart).

What these examples show is that success invites competition, shrinking profit margins, and reducing monopoly power. Thus the reinvestment rate assumption, particularly on blockbuster products, typically does not hold and can be drastically overstated. This means that blind application of IRR can lead to bad capital budgeting decisions or outcomes that produce less profitability after-the-fact than expected.

The reinvestment rate assumption and NPV: What about the reinvestment rate assumption for NPV?

![]()

This assumption applies equally to projects considered to have great sales potential or ones of just average sales potential. Clearly this is a more conservative reinvestment rate assumption than that used for IRR. The philosophy of the NPV method is that the cash flows can be put to work at an average rate of return = WACC, no more. While, in some cases, this "average rate of return" assumption may turn out to be false, it leads to better capital budgeting decisions in the long run. After all, if the firm can't reinvest projects' cash flows at the WACC then they shouldn't be in business.

Conclusion: NPV is considered superior to IRR since it makes a more conservative assumption about reinvested cash flows.

Irrespective of the comments in the previous paragraph I advise anyone engaged in capital budgeting to carry out as many methods as possible. Each method sheds a different perspective on the expenditure decision by bringing additional information to the capital budgeting task. Additionally once you have the projected cash flows for a project or projects in Excel, the pure number crunching is a keystroke away. Finally, most of the time all methods will give the same accept or reject decision.

A few capital budgeting problems

The Payback Method

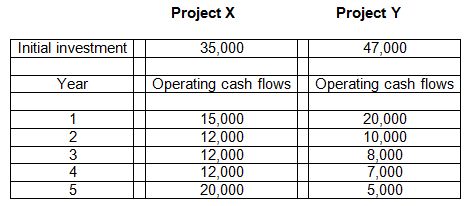

The initial investment amount and operating cash flows for Projects X and Y are listed below in dollars:

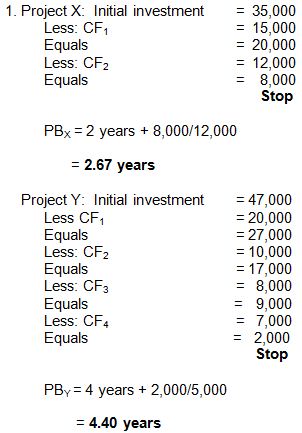

1. What is the payback of each project?

2. If the projects are independent and management sets payback at three years (X years), which project(s) should be accepted?

3. If the projects are independent and management sets payback at two years (X years), which project(s) should be accepted?

4. If the projects are mutually exclusive and management sets payback at two years which project should be accepted?

Solutions

2. If the projects are independent and management sets payback at three years Project X should be accepted and project Y should be rejected.

3. If the projects are independent and management sets payback at two years neither project should be accepted.

4. If the projects are mutually exclusive and management sets payback at two years Project X should be accepted and Project Y should be rejected. For two mutually exclusive projects take the shortest payback assuming payback is within the maximum payback period.

The NPV method

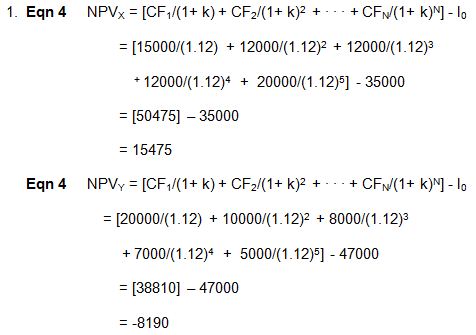

The initial investment amount and operating cash flows for Projects X and Y are listed below in dollars:

1. If the WACC is 12% what is the NPV for each project?

2. If both Projects X and Y are independent which project(s) should be accepted and which should be rejected?

3. If the two Projects are mutually exclusive, which project should be accepted?

Note: You should work these problems using your calculator following the instructions in Appendix 2. For explanatory purposes the solutions presented here use Eqns 4 where the initial investment is placed at the end of the equation as I0.

Solutions:

2. If both projects are independent Project X should be accepted since it has a positive NPV and Project Y should be rejected since it has a negative NPV.

3. If the two projects are mutually exclusive Project X should be accepted and Project Y should be rejected. Note that Project Y would be rejected whether the projects are independent or mutually exclusive since its NPV is negative.

The IRR method

The initial investment amount and operating cash flows for Projects X and Y are listed below in dollars:

Here you do need to use your calculator is indicated in Appendix 2.

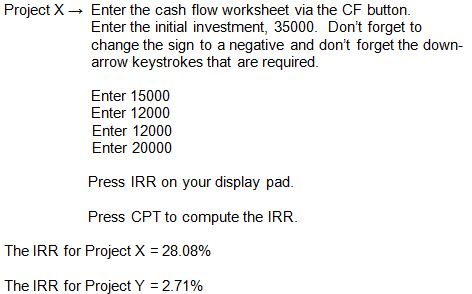

1. What is the IRR for each project?

2. If both Projects X and Y are independent which project(s) should be accepted and which should be rejected?

3. If the two projects are mutually exclusive, which project should be accepted?

Solutions:

1. Here is a brief review of the steps to follow using Appendix 2:

2. Project X should be accepted since its IRR is greater than the WACC. Project Y should be rejected since its IRR is less than theWACC.

3. If the two projects are mutually exclusive, Project X should be accepted since its IRR is greater than the WACC. Project Y should be rejected since its IRR is less than the IRR for Project X and since its IRR is less than the WACC.

Summary: Both the NPV and IRR methods give the same accept/reject decision. The Payback method tends to suggest Project X should be accepted and Project Y should be rejected.

Content ©2012. All Rights Reserved.

Date last modified: October 4, 2012.

Created with SoftChalk

![]()