Money Flow - Part 5

Stastics & Risk Management

Money Flow - Part 5

Stastics & Risk Management

Dividend policy and management's financing and capital structure mix:

In order to maximize share price the firm's dividend policy must be co-determined with three other value-impacting variables controlled by management:

1. The firm's investment policy;

2. The firm's financing mix;

3. The firm's capital structure. On a practical level it is impossible to change one variable without considering the others.

For example, a firm that has a high dividend payout must consider the fact that cash resources are being used to provide a current return to shareholders. Therefore, these funds are not available for longer-term investment spending today. Likewise, a firm committed to a high dividend pattern may have to finance its cash operating needs by issuing more debt and/or equity if internally generated funds are insufficient. In turn, the resulting debt-or-equity financing mix will affect the firms capital structure (the proportion of its assets financed via debt or equity). Clearly, decisions about the firm's dividend policy cannot take place in a vacuum if share price is to be maximized.

Dividends and the impact on external versus internal financing

Number (2) above (the chosen financing mix) refers specifically to dividend policy and the distinction between internal versus external financing. From Part 2 of the Money Flow module on financial statements we learned that earnings could either be retained or paid out to stockholders.

Earnings that are retained become a form of internal financing. This cumulative amount shows up on the balance sheet as Accumulated Retained Earnings; on the left-hand-side of the balance sheet these earnings are reflected in assets. Sometimes internal financing is sufficient to fund the firm's operating growth and dividend needs; sometimes it's not. Thus the dividend decision (after allowing for the investment and capital structure decisions) can significantly impact the firm's external financing requirement via the need to issue more debt and/or more equity. Keep in mind that while dividends are written off to retained earnings on the balance sheet, they are paid out of cash. This may sound like some firms actually borrow or issue new stock, so as to pay dividends to existing stockholders. While not overtly carried out, this practice does occur indirectly when the firms investment decisions have been made and the firm then indirectly channels some of its borrowed funds to cash dividends.

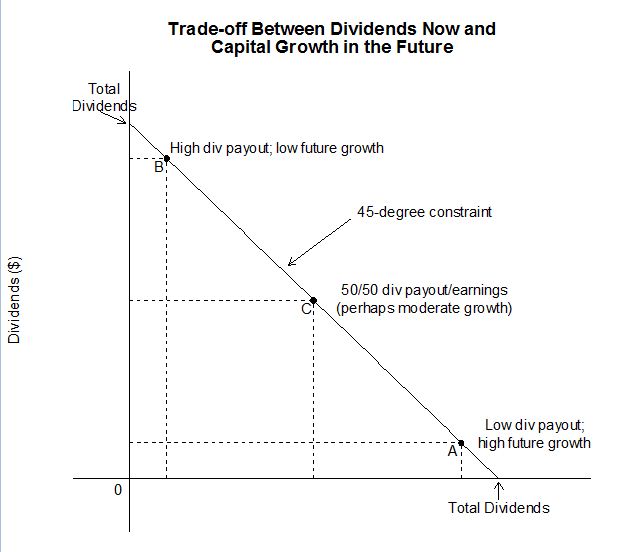

As mentioned in the section "Understanding a few things at the outset"; many firms in a strong growth phase tend to plow earnings back into the company. Doing so constitutes internal financing. As a result they are forced to seek external financing if they wish to simultaneously pay dividends and spend on core investment. This is especially true if internally-generated funds will be insufficient to undertake new projects. Unfortunately Figure 1 does not indicate how much external funding is involved in management's dividend decision. However, the empirical record shows that when growth prospects are extremely good and payout is close to 0%, firms will then engage in external financing.

Content ©2012. All Rights Reserved.

Date last modified: September 19, 2012.

Created with SoftChalk

mobile page

![]()