Money Flow - Part 5

Stastics & Risk Management

Money Flow - Part 5

Stastics & Risk Management

Empirical evidence suggests that a firm's dividend policy tends to attract different groups of investors (different clienteles), depending upon how these investors wish to receive their total rate of return on their investment in the company's stock. Specifically, those investors who want high current investment income and expect to forego anticipated long-term capital gains would buy the stocks of firms with a record of high dividend payouts.These might be bird-in-the-hand-type investors. Conversely, those investors who are in their prime earning and savings years might elect to own the stocks of firms with a record of low (or zero) dividend payouts.

This would serve two purposes:

1. These stockholders would defer taxes on dividends not paid out

2. The foregone dividends could be plowed back into the company to earn a longer-term expected capital gain. This group might be in the tax-preference group of investors. This group's philosophy is that since they're wealthy as heck and don't need the cash (remember the proverb, "Poverty Sucks"), let the firm act as an agent for tax-deferred long-term growth. Research shows these different investor preferences regarding payout patterns can be quite powerful. For example, see R. Pettit, "Taxes, Transactions Costs, and the Clientele Effect of Dividends," Journal of Financial Economics, Dec 1977, pp 419 – 436.

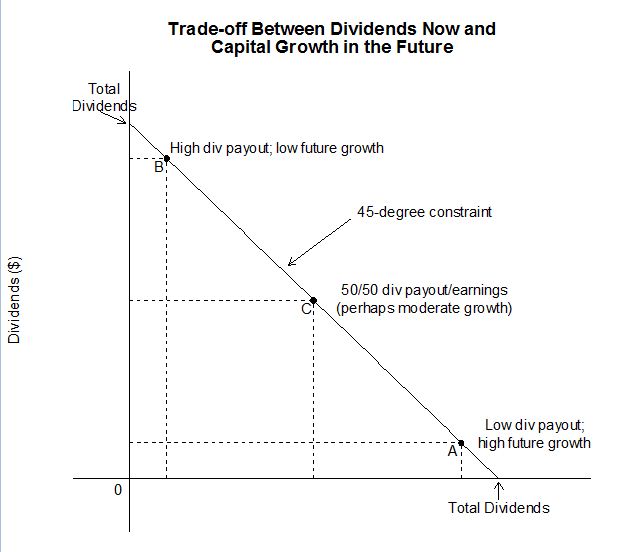

The clientele effect can be effectively demonstrated by referring once again to the tradeoff graph shown in Figure 5-1. If a firm fits the dividend profile implied by point A (low dividend, high expected capital gain) it would tend to attract investors less interested in current dividend income and more interested in capital appreciation of the firm's stock. Conversely, if a firm fits the dividend profile suggested by point B (high dividend, low expected capital gain), it would tend to attract a clientele more desirous of high, steady, current income.

Clearly, once a firm establishes its payout pattern and attacks a given clientele, a shift in dividend policy would be ill-advised. While such a shift could occur, it would be tremendously disruptive to shareholders' portfolios. First, it would alter the manner in which total return would be received. Some retired shareholders who had elected high payout firms would be faced with lower current income and the prospect of not being around in the distant future ("not being around"—I wonder what that means?) to enjoy the expected capital gain return that a low payout profile entails. Younger investors who had elected to go with low payout firms that switched to a high payout would now be faced with a higher tax burden and the prospect of not having the expected long-term capital gain. While investors could subsequently switch to firms that offered the payout profile they desired, such changes would entail brokerage fees and general hassle costs. It's quite probable that a firm that caused its clientele to weather these disruptions might be rewarded with a lower stock price for their efforts. Typically, we see that once a firm establishes its payout pattern they try to stick with it because they have attracted a given stockholder base.

So the general rule that we see in practice is one where the dividend policy, once established, is not subject to too much alteration. The clientele effect does a very good job in explaining this empirical finding.

Content ©2012. All Rights Reserved.

Date last modified: September 19, 2012.

Created with SoftChalk

mobile page

![]()