Money Flow - Part 5

Stastics & Risk Management

Money Flow - Part 5

Stastics & Risk Management

From the logic about the clientele effect given in the section: A brief discussion of some dividend theories, we inferred that managers try to follow practices that smooth their dividend patterns over time so that dividend stability is achieved. Well there is another, perhaps more subtle reason why managers prefer to smooth dividend payouts. It's based upon the twin concepts of asymmetric information and the signaling aspect of dividend announcements.

The signaling aspect associated with dividend practice and dividend announcements: Management's decision to pay or not pay dividends can create (unwarranted) shareholder expectations about the future earnings potential of the firm in an asymmetric information setting. Asymmetric information can occur when management has more (inside) information about the firm than stockholders have access to. Asymmetric information outcomes make sense since managers are down in the trenches on a day-to-day basis while stockholder/investors are (usually) not. The resulting information imbalance is at the center of the signaling hypothesis. Simply put, dividend policies and (especially) unanticipated changes in payout can carry a strong informational content that management should be aware of.

Consider the case where the firm has followed a particular payout policy for a long time, when it is somewhat secretive about its plans or strategies, or when stockholders don't make an effort to keep up on the factors impacting the value of their stock investment. In this case signaling will be most pronounced when an existing dividend policy is changed unexpectedly.

Thus, it's the change in policy, not the policy per se, which elicits a good or bad message about the firms future prospects. For example, an announced dividend that's (say) 5 percent higher than the norm can signal to stockholders that management is anticipating good future earnings. Share price will rise. Conversely an unexpected decrease in payout can signal that the firm's prospects are not good—why else would management cut dividends? Stock price will fall. This phenomenon has been reasonably well documented in the literature and makes intuitive sense. For example, see E. Dyl and R. Weigand, The Information Content of Dividend Initiations: Additional Evidence, Financial Management, Autumn 1998, pp 27 – 35.

An example: Consider Mr. Jim who's a stockholder in Company X, a microchip manufacturer. At the end of every quarter he receives his dividend check like clockwork. One quarter though his check is not received; it's been replaced with a brief message from the firm's Board of Directors stating that dividends will be suspended for an indefinite period of time. Mr. Jim wonders what's up. He calls his broker, Clyde, who doesn't have much information about the situation (typical of many brokers who are only interested in sales).

Since Clyde originally sold the stock to Mr. Jim a few years ago he attempts to comfort Jimbo with the following possibility: Perhaps the firm has come upon an unexpected technological breakthrough in microchip production. Logically Company X wishes to develop this positive NPV project before others do. To do so they need ready cash. Result: No dividends for the foreseeable future. Now if this scenario is true it means that Company X's stock will be appreciating as the market learns of the breakthrough. If this is the case, Mr. Jim would be happy and not question the dividend cut. But he doesn't really know.

But Clyde also tells him that the reverse could be true: Maybe the EPA has just found the firm in violation of important environmental laws and the firm must either invest in new environmentally-friendly equipment or face a big law suit. In this second situation Mr. Jim would surely be unhappy and sell the stock of Company X immediately if this scenario is true. But again, he doesn't know.

That's asymmetric information at work. It's the uncertainty about the worth of one's investment as produced by lack of information about dividend changes that can really hurt a company's stock price.

While we do see firms trying to keep shareholders informed about any changes in dividend policy, it's still difficult to avoid bad signals emanating from a change in dividend policy even if the policy change is one that will enhance shareholder value.

Dividend smoothing and dividend stability: Management wants to avoid the type of situation just described. Hence the record shows that firms tend to follow a dividend policy that smoothes dividends even in the face of low (or negative) earnings. A policy of dividend stability is what we observe in practice precisely because of the informational content that accompanies dividend announcements and, more importantly, unanticipated alterations in dividend announcements.

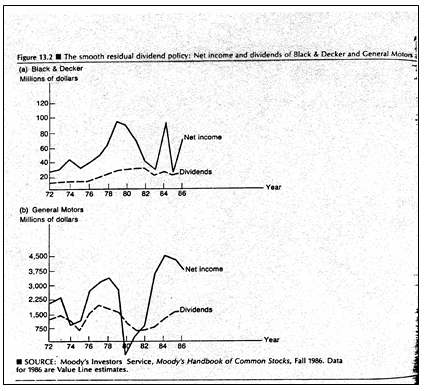

Figure 5-2 provides empirical evidence in support of the signaling hypothesis that firms prefer to keep their dividends stable thus avoiding unwanted information by-products.

Figure 5-2

Here we see a time plot of net income and dividends for Black and Decker and General Motors from 1972 through 1985. This was a fairly turbulent period in U.S. economic history with oil and agricultural supply shocks occurring in 1973 – 1975 and extremely high inflation and interest rates in 1979 – 1981. These conditions are in part responsible for the volatile time plots of net income for both Black and Decker and GM that you see in the Figure. However, while dividends for both firms tended to oscillate a bit over the time period, it is obvious they were much smoother than net income. Note that GM, who was known for always paying a dividend, paid a dividend in 1980 in spite of negative net income. You can imagine what GM shareholders would have thought about the company (and what would have happened to its stock price) during this economically-troubled period had GM halted dividends in 1980. (I refrain from commenting on GM's recent financial situation as it did not apply when the data for this graph was assembled.)

It is relevant to combine dividend smoothing with the previously-discussed material on the residual theory of dividends. It is precisely because a residual theory, if followed to the letter, would produce unwanted signals that the residual policy is not followed in practice.

Content ©2012. All Rights Reserved.

Date last modified: September 19, 2012.

Created with SoftChalk

mobile page

![]()