Ethics and finance

Background: Ethics is defined as behavior consistent with established standards of conduct and moral behavior. In recent years there has been a strong movement to enforce ethical behavior on corporate conduct and governance. Compliance has become an overriding issue in the financial community as well as for society at large. Recent corporate examples of ethical violations that were subsequently turned into legal sanctions are violations related to Enron, Tyco, WorldCom and Apple. The ethical (and legal) violations of these firms attracted widespread publicity resulting in a negative impact on these firms' wealth and viability. Business managers are now expected to establish a written code of conduct and to enforce what are called business ethics—standards of conduct and moral behavior which rule the company's business activities.

Determining ethical behavior: Unethical behavior is not necessarily illegal behavior in a statutory sense. So then, what constitutes behavior that meets ethical guidelines from the standpoint of the modern corporation? R. A. Cooke is a well-know ethical theorist. He suggests the following questions be used to determine the ethical standing of a decision from the corporate perspective:

- Does the action unfairly single out an individual or group or does the action affect the morals or legal rights of any individual or group?

- Does the action conform to accepted moral standards or are there alternative courses of action that are less likely to cause actual or potential harm?

- Does the firm have any overriding duties to any stakeholder, or will a decision benefit one stakeholder to the detriment of another? If so, how should this conflict be remedied?

Up-front: Let's recognize upfront that constraints on ethical behavior have always provided some type of framework for dealing fairly with parties to commercial transactions as implied by the above questions. However, as the conduct of business has become more complex and fast-changing, what is required by law (i.e., what is statutorily mandated) and the behavior that is expected ethically has become clouded and ambiguous. Unfortunately, only when a particularly egregious act or scandal comes to light has action been taken to enforce ethical behavior. The problem is that enforcement has tended to be re-active rather than pro-active. Some examples of serious breeches of ethical (and legal) standards violations have been accounting and earnings mis-management, biased financial forecasting, insider trading, overt fraud, excessive executive compensation programs, stock options backdating, kickbacks, and actions which only serve to entrench management.

A particularly noteworthy instance of financial statement fraud relates to the 2002 financial reporting by WorldCom. At the time WorldCom was the second largest telecommunications company in the U.S. In 2002 it recorded ordinary operating costs as capital expenditures instead of ordinary operating expenses. This removed $3.8 billion of expenses from the income statement and placed these expenses on the balance sheet where they would be slowly depreciated over time. This financial gymnastic resulted in a massive overstatement of net income and cash flows. Investors and banks were fooled. The accounting firm Arthur Andersen (WorldCom's auditor) was faulted for not detecting the fraud. This is an example of overt accounting mis-conduct.

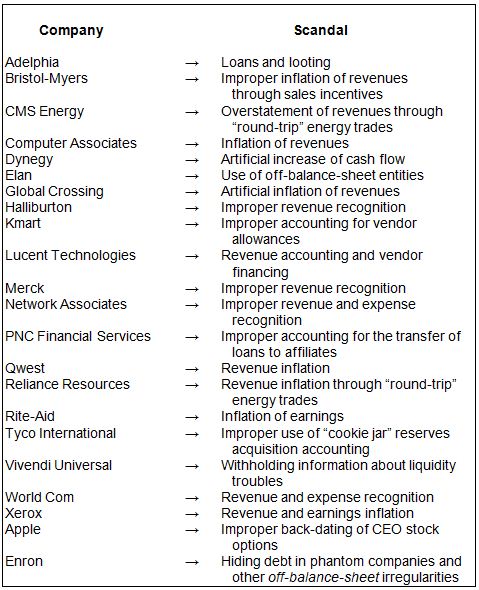

Some other overt and covert examples of accounting violations between 1998 and 2008 follow in Table 10-2. Clearly all these qualify as ethical violations. Some violations subjected the guilty firms to legal sanctions as well. This is not a complete list as some allegations are still pending as of 2011. If we were to include post-2007 incidents many investment banking houses and certain quasi-government agencies related to the home lending debacle (e.g., Fannie Mae and Freddie Mac) would be listed along with the Bernie Madoff pyramid scheme.

Table 10-2. Prominent business sandals revealed between 1998 and 2008 ( Source: Bloomenthal, 2008)

Digression:The Sarbanes-Oakley Act of 2002 - The types of accounting violations listed above have resulted in many new legal standards. Perhaps the most well-known is the Sarbanes-Oxley Act of 2002 (SOX). This Act was the result of numerous corporate misdeeds deriving from false disclosures in financial statements and the continued acceptance of conflicts of interest between corporations and the analysts charged with judging performance and reporting to shareholders. The outcome of the SOX legislation was to audit and eliminate financial disclosure and conflict of interest violations. It also led to stiff penalties against analysts and corporate managers that committed fraud.

1. The specifics of the SOX legislation are:

2. established an oversight board to monitor the accounting industry;

3. tightened audit regulations and controls;

4. toughened penalties against executives who commit corporate fraud;

5. strengthened accounting disclosure requirements;

6. established corporate board structure guidelines.

Enforcing the SOX legislation has not be costless. Adherence to SOX standards has placed huge financial burdens on a company's reporting requirements (it's also increased the demand for accountants!). This burden translates to higher reporting expenses and ironically these costs must be borne by the stockholders. Presumably the benefits for stockholders (greater honesty) will outweigh the costs. Whether SOX and like legislation will be effective is still unknown at this time. However, in the public's eye, professional practice is now judged by a keener perception of the spirit of ethical behavior.

Both the letter and the spirit of the law: The overriding goal of ethical standards is one of motivating and auditing business activities so that these activities adhere to both the letter of the law (the statutory aspects of behavior) as well as the spirit of the law. Clearly there is a gray area between the legal constraints on behavior and the "do what's right" intent of the law. A strictly-followed code of business ethics is supposed to ameliorate this ambiguous gray area in business interaction and decision-making. This is often not the case in today's business climate.

Ethical behavior and the link to corporate governance: Corporate governance defines the organizational links existing between the firm and all entities who share a direct economic link with the welfare of the firm. This group is generally referred to as stakeholders and is broader than the term stockholders. (Stakeholders are not listed in Figure 10-1.) Besides stockholders these groups include bondholders, employees, customers, suppliers, and society at large. Key corporate parties including the Chief Executive Officer and the firm's Board of Directors bear the responsibility of maintaining appropriate legal and ethical ties between these entities and the overall corporate mission.

Maximization of stockholder wealth: Prior to ethics becoming more prominent in business management the supposed aim of corporate governance as stated in the corporate mission statement was confined primarily to the welfare of the common stockholder. In this light management's job was to maximize stockholder wealth as reflected in a rising intrinsic stock price over time. To a large extent ethical behavior applied to stakeholders at large was taken for granted. The idea was that since stockholders owned the firm and elected the Board of Directors and managers, we could assume corporate administrations would automatically act in the best interests of the stockholders by doing things that maximized stockholder value. Competitive market forces would force managers to undertake actions that were consistent with shareholder wealth maximization.

Ethics, stock price maximization, and social welfare: This idea in turn led to the belief that actions which maximized stock price were also consistent with social welfare decisions. That is if a firm maximized its intrinsic stock price, society in the end would benefit as well.

This reasoning is based upon three premises:

1. Since over 50% of all U.S. households own stock (either directly or through retirement funds, life insurance companies, and mutual funds) when managers maximize stock price they are simultaneously maximizing social welfare

2. Stock price maximization in combination with market competition keeps managers conscious of production costs as well as sales. By so doing the consumer benefits

3. Employees benefit as well since by maximizing stock price companies are able to attract and retain the best of the workforce thereby promoting corporate success.

Stakeholders, not just stockholders: Collectively these ideas have led to the broader view that the firm's actions should be aimed at the stakeholder, not just its stockholders. This broader perspective prescribes that the firm should make a conscious effort to avoid actions that could be detrimental to the wealth position of its broader stakeholder constituency. This view is considered to be the "socially responsible" frame of reference for public-held companies. It is considerably wider in corporate responsibility than a strict stockholder wealth maximization view point since the latter perspective does not recognize the negative spin-off activities that can impact social welfare.

Financial decisions: An automatic route to ethical decisions? Since this belief was born (in the early 1950s) the stock of most corporations has become widely held. This fact has tended to promote corporate managements to act in a sometimes capricious and autonomous fashion. Additionally some management teams have developed well-entrenched infrastructures that have tended to vote for management and against the best interests of the stockholders on corporate decisions.

The widespread financial and legal mis-management deeds of U.S. corporations that occurred from 1980 to the present has caused the financial, legal, and political communities (and the public at large) to re-visit the corporate ethical landscape. The general conclusion today is that blind adherence to the stockholder wealth maximization objective will not automatically lead to business decisions that are in line with the ethical dictates demanded by an informed society nor to an improvement in social welfare.

Perhaps the most glaring example of an ethical misalignment between these conflicting interests is the on-going contest between corporate decisions and the environment. As environmental sustainability has gained attention, government has had to step in and curb corporate negative spillover effects, effects that were not supposed to occur under the banner of stockholder wealth maximization. The corporate profit versus eco-friendly production story is still unfolding, but it is safe to say that corporations left to their own devices would probably make decisions that run counter to the environmental impact those decisions would render. Ethics would be out of the window. As a result government intervention has stepped in to regulate corporate behavior that is deemed socially detrimental. Simply put, if government forces corporations to internalize their social costs, then these costs must reduce the "bottom line" for the stockholder. To the extent that firms can pass on these costs to consumers in the form of higher prices, consumers ultimately pay these production-produced social costs.

The place of private property rights in ethical behavior: A property right might be thought of as a right, enforced by law, to act based upon private property ownership. The place of legal property rights presents a broader view of the ethics debate and is centered on society as a whole rather than on individual stockholders or stakeholders.

At the root of much of the "environment versus corporate profit" debate is the private ownership (or control) of the Earth's natural resources (e.g., clean air, potable water, lack of noise and light pollution, etc). Production usually carries with it unintended by-product consequences (i.e., a polluted planet in one form or another). Profits require control of natural resources. This control can be obtained via the law under the moniker of private property rights. In this scope of viewing production, ownership gives control to the owners to use the resources in the most profitable manner. If the by-products of control could be relegated to the immediate producers all would be fine. Unfortunately this is not the case. Most types of production carry negative spillover costs (i.e., externalities). By definition and "externality" is a negative impact of production that affects others not involved in the production process. (If you live downstream from a dairy farm you know what I mean!)

Producers argue that private property ownership gives them the right to produce. However, it does not give them the right to spoil the world of third-parties. A solution is to internalize the negative spillover effects of production by forcing producers to pay the "social costs" of production. Doing so raises the costs of production. If these costs are passed on the public in the form of higher prices production can supposedly carry on and all is well. This sounds very similar to the above discussion, Financial decisions: An automatic route to ethical decisions? It is.

It's simple, right? Wrong; unfortunately it's not that simple. It is extremely difficult (or impossible) to internalize all production spillovers. Thus, negative externalities result in final prices that are too low, production that is too high, and an existence that is polluted. Pure and simple, this is an ethical issue even though it's not related to accounting mis-management or lavish company parties that do not benefit the stockholder. What maximizes stockholder wealth is long-term cash flow and the very financial management decisions that maximize cash flow are the ones that try to avoid (politically or otherwise) internalizing negative spillover costs. Result: Society bears the cost. Hence the apparent contradiction often seen in the finance literature and the statement: " By maximizing stockholder wealth we will maximize social welfare." The validity of this statement should be questioned.

You make the call . . .

As long a there are negative spillovers to production, private property can never be private—it's all public. In fact if you want to be downright ludicrous about the argument, in today's pressed-for-space world there can be no private property—what I do in my back yard will drift over and affect you in your back yard. (Now if you want to lean over the back fence and "drift" me a cold beer I will shut up!). While government controls can try to limit this contradiction, to do so runs into tremendous political and economic pressure. Government usually fails to do the job adequately. Then you are down to a "jobs or the environment" mentality. To argue for jobs is "American"; to argue for the environment is "un-American."

The Agency Relationship in finance: Related to the topic of ethics and business decision-making is the agency relationship in finance. In spirit this relationship is discussing the same basic philosophy that connects standards of conduct to corporate behavior. It is not new to finance; rather it has been adopted by the finance literature from other areas of human interaction (primarily politics). As we will see, an "agency perspective" of business ethics lends a bit more focus to the standards of conduct discussed above.

The principal/agent relationship: The agency relationship is based upon the principal/agent affiliation. A principal hires (or elects) an agent. Implicit in the contract is the understanding that the agent will act in the best interest of the principal. As long as this is the case the agency relationship is not being violated. Being the owner of the company the stockholder is the principal; the financial manager hired by the principal assumes the role of an agent. Excluding other possible production-produced social costs, if the financial manager's decisions are ones that increase the intrinsic price of the stock over the long-run then the principal/agent affiliation is being maintained.

Separation of ownership and control: In corporate American there is a natural separation between the owners of the firm and those that control the firm on a day-to-day basis. In most large companies the firm's managers generally own only a small percentage of the company's stock. The stockholders own the firm; the managers control the firm. This separation of ownership and control stems from a natural division of labor which benefits both groups. Managers know how to run the company while stockholders supply the financial capital and collect their return on investment. While stockholders can vote on major company issues, many do not or do not know the specifics to make informed decisions. If managers operate such that major decisions maximize stockholder wealth separation of ownership and control causes no ethical problems. However, this is often not the case particularly when stockholders are indifferent about the everyday affairs of the business.

The agency problem: An agency problem occurs when agent/managers do not act in the best interests of the principal/stockholders. Separation of ownership and control, while it has obvious benefits, allows the agency problem to occur since it presents a potential conflict of interest. That is the over-riding objective of stock price maximization that can be placed behind any number of conflicting managerial goals. For example, managers may act to increase his/her own welfare in the form of increased salaries, add more benefits or perquisites in the form of lavish parties or vacations. Other forms of conflicts would be managers acting too conservatively about investment spending, increasing their job security by hand-picking the members of the Board of Directors, or adding assets simply to reflect personal hubris rather than to add to stockholder wealth.

Separation of ownership and control and altered incentives: The above list of agency violations represents overt management actions which lead to violations of the agency relationship. However the cause of agency violations can be more subtle and more indirect. These relate to the fact that separation of ownership and control can serve to alter the incentive structure of managers to act in the best interests of the stockholders.

The idea is simple: If managers own most of the company they will be inclined to make decisions that will increase the wealth of the company; if managers own only a small percentage of the company the incentive to act in the best interests of the stockholders can become diluted.

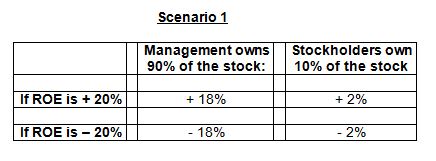

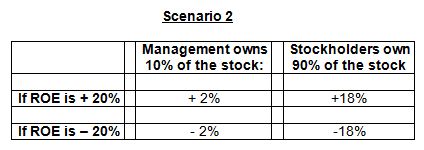

This idea is demonstrated in the Table 10-3a.The upper section shows Scenario 1; the lower section shows Scenario 2. In Scenario 1 management owns 90% of the company with stockholders owning the remaining 10%; in Scenario 2 management owns 10% of the company with stockholders owning the remaining 90%. For both scenarios we assume that there are only two earnings outcomes for the coming year, a Return on Equity (ROE) of +20% or an ROE of -20%.

Table 10-3. Two incentive-altering ownership structures

In Scenario 1 if management does a great job in financial decision making for the coming year such that ROE turns out to be a healthy +20% they keep most of the return (18%) and stockholders only share +2% of the ROE. However, if they make lots of bad decisions such that ROE results in a -20% management suffers most of the loss in equity (a negative 18%) and stockholders only bear a minor 2% loss.

Now let us assume that the managers sell off 80% of their stock in a public offering (this might occur if they decide to take the company public in an IPO). This will result in management owning 10% of the stock and outside stockholders owning the remaining 90%. We assume the same ± 20% ROE outcomes for the coming year.

One can see how the incentives of management would be altered with the shift in ownership percentage. Namely, if management does a great job and returns a +20% ROE they only garner +2% of the performance results for their efforts; the outside stockholders take the other +18%. Conversely, if management falls down on the job for the coming year such that the company returns a negative 20% ROE, management only suffers a 2% ROE loss; the stockholders bear the brunt of the bad decision-making with a negative 18% ROE.

Conclusion: Separation of ownership and control can result in subtle effects which alter the performance incentives of management to maximize stockholder wealth. Keep in mind that these types of ownership incentive-caused changes in managerial decisions should not be categorized as "good" or "bad" per se. Management decisions in this context are clearly in a different category than the overt cases involving conscious mis-deed and fraud. Rather they result from the normal tendency to do a better job when the job-doer will benefit directly from the end-product.

Methods to deal with the agency problem: There are both positive and negative methods to help align management efforts with those of the stockholders and stock price maximization.

Some positive methods are:

- Managerial compensation: Tie management's salary to performance though salary bonuses.This method would clearly connect management decision-making with stockholder interests.

- Performance shares: Performance shares are the gifting of company shares depending upon the company's actual performance and continued service of the manager(s). Again, this tactic would tend to align management action with wealth maximization.

- Executive stock option plans: These plans allow managers to purchase stock at some future time at a given price established today. The incentive is the future capital gain that can be achieved if management's performance is reflected in the market price of the stock. Stock option plans clearly have the intent of offering management the "carrot" which will also serve to advance the objectives of the stockholders.

Some negative methods are:

- Termination by stockholders: This can occur if a group of dissatisfied stockholders votes the manger(s) out.

- Intervention by large institutional investors: Since institutional ownership can amount to 5 percent of the company's outstanding stock, institutional money managers have the clout to expel managers for continued bad performance. In this situation the institutions act as lobbyists for the interests of the stockholders at large.

- Hostile takeover: A hostile takeover can be precipitated if the firm's stock price in the market gets too low due to bad management. This possibility represents a negative motivation for management to excel.

The agency relationship between stockholders and bondholders: Bondholders lend the company money based upon an expected risk level. If subsequent action by the company leads to a riskier business environment for the company than initially impounded in the bondholders' required rate of return this represents a violation of the agency relationship between stockholders and bondholders. (Here we recognize that stockholders, not managers, are the principals.)

Recall that bondholders receive a fixed cash interest payment. This payment is not tied to company performance as is the return to stockholders. A good management decision that leads to increased return will not benefit bondholders. However, a bad decision that places the company at risk of default stands to erase the bondholders' promised rate of return. So good decisions and higher rates of return accrue to the stockholders. Conversely the result of bad decisions is the loss of the bondholders' investment. This asymmetric risk outcome is not one that bondholders bargained for, but must bear. To counter this possibility the bondholders typically can resort to a bond issue's indenture contract to protect their investment from bad management decisions. However, it is often the case that bondholders can lose their entire investment if a bad decision bankrupts the company.

Summary comments on the agency problem in finance: As you can see the agency problem in finance is just a re-worked ethics situation. While headlines may indicate otherwise, research studies show that the goals of stockholders and those of management do not diverge significantly. However as inferred from the discussion above, the goal of blindly aiming at stock price maximization can produce lasting and significant social spillover costs. These represent ethical violations which can harm stockholders' interests. We also mention that controlling agency problems is not costless. Agency costs are the costs borne by the stockholders. These costs include increased monitoring, bookkeeping, legal fees, bonding costs, and stock options that are exercised at a strike price that is lower than the selling price.