Dividend Theories

In this section we describe some prevailing dividend theories and hypotheses. Later in this module we will discuss some actual real-world dividend policies followed by corporations. Do not confuse dividend theories/hypotheses with practiced dividend policies—they are not the same.

A dividend theory is a formulation of an apparent relationship which purports to explain a connection between dividend patterns and various causal factors impacting these patterns. Practiced dividend policies on the other hand are based upon observed corporate behavior describing its payout procedures. Practiced policies often cannot be fully explained by pure theory.

The key question: For dividend theories the key question is, "Does the dividend policy implied by the theory really have any impact on the firm's value?" In other words, does it cause firm value? This more abstract question has been explored by Professors Modigliani and Miller (MM). [See M. H. Miller and F. Modigliani, "Dividend Policy, Growth, and the Valuation of Shares." Journal of Business, Oct 1961, pp 411-433 and others.]

The method to the MM reasoning is simple: MM make some ridiculously unrealistic assumptions about how corporations pay dividends. They (and other subsequent researchers) then slowly relax these assumptions so as to make them more realistic. In so doing the convoluted theory provides some useful insights into the way the world really works.

We will discuss four prevalent dividend theories:

1. The MM dividend irrelevance theory

2. The residual dividend theory

3. The bird-in-the-hand theory

4. The tax preference theory

Dividend Irrelevance Theory: The MM dividend irrelevance theory states that the firm's dividend policy has no impact on firm value or its stock price. The implausible set of assumptions upon which this theory is based are that financial markets are perfect and shareholders can construct their own dividend policy simply by buying or selling shares in the market as they desire. If they want cash, they can (without brokerage costs) sell shares; if they don't they can hold on to their shares. The irrelevance theory also assumes that there are no brokerage fees or capital gains taxes. Finally, they assume away such things as voting control preferences and any signaling effects resulting from dividend payments. Once these assumptions are relaxed we see that dividends indeed do matter.

Given these assumptions, though, they conclude that the firm's value is determined solely by its basic earning power and its business risk—that is its ability to produce risk-adjusted cash flows going forward. Thus the value of the firm depends only on the productivity of its assets, not on how the cash flow from these assets is split between dividends and retained earnings. What surfaces is the conclusion that a firm's dividend policy is irrelevant in determining its value. That's their argument. We could put this in math terms but let's not. Whew !

The logic? There must be some logic here. MM reason that a firm's decision about dividends is often mixed up with other financing and investment decisions. For example, say a firm decides to lower its dividend policy because management is optimistic about the firm's future and it wishes to retain earnings for new investment. In this case the dividend policy becomes a by-product of the firm's capital budgeting decision. Then, if the firm's stock price falls because dividends are cut so as to undertake new investment spending, is this price drop due to the (new) investment decision or to the dividend decision? In another situation a firm might finance capital expenditures largely by borrowing. This then releases cash for dividends and the firm's stock price rises. In this case the firm's dividend (and stock price increase) are by-products of the financing decision.

What these examples illustrate is that in order to truly define a firm's "dividend policy" it is necessary to isolate the policy from the investment and financing decisions. In effect the only way to observe the true relationship between dividend policy and stock price is to

1. first decide on the investment and financing decisions, and then

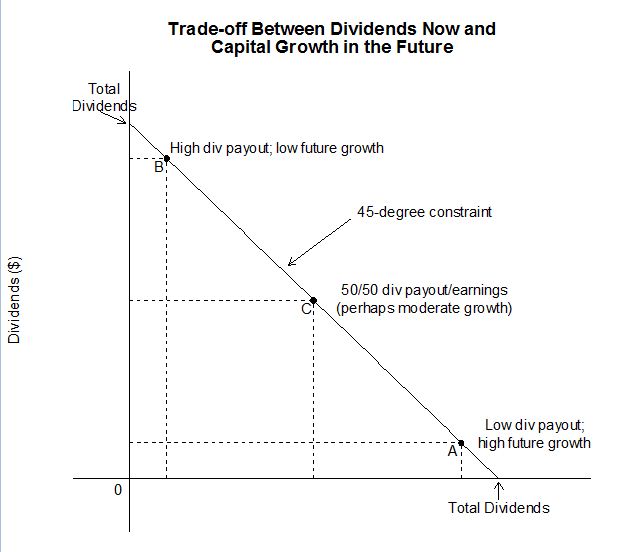

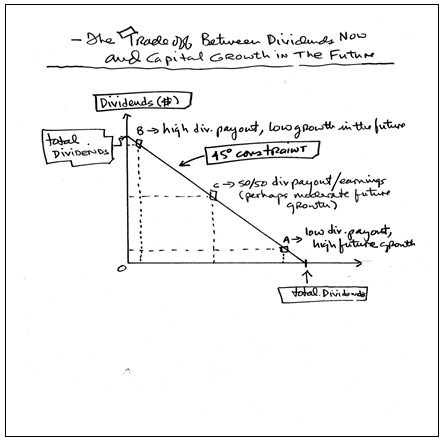

2. issue stock to finance the dividend payment. This leads to a more focused definition of dividend policy, one that emphasizes the budget constraint described graphically in Figure 5-1 which shows that that a true dividend policy is one where there is a tradeoff between retaining cash flow on the one hand and issuing new shares and paying out cash dividends on the other. However, once the investment and financing decisions are made, the MM version of the "dividend decision" will still leave the value of the firm unaffected. In this stylized MM world, dividends don't matter—they are irrelevant.

Figure 5-1

The residual theory of dividends: Now that we have described the idea of dividend irrelevance it's easy to talk about the residual theory of dividends. This is not a direct MM creation but it comes to the same conclusion about dividend irrelevance.

The theory suggests that the dividend paid by a firm should be viewed as a residual – the amount left over after all acceptable investment opportunities have been undertaken. But this theory is a bit more involved than this simple idea.

Consider this. Let's define the firm's target capital structure as one where the proportions of debt and equity maximize stock price. What if there was a dividend policy that simultaneously considered the firm's target capital structure, its pending capital investment spending program, and the amount of equity needed to fund these investments. Let us also assume the firm will use reinvested earnings rather than new stock issuance to obtain the appropriate equity amount to maintain the target capital structure. Finally the firm will pay dividends only if there is more earnings than needed to support the firm's target capital budget spending program? "Wow," you would say, "That's great! Gim'me some shares."

Well, the residual dividend model prescribes such a dividend policy. As the word "residual" suggests, dividends are what's left over after the firm has paid all its bills and undertaken all profitable (i.e., positive NPV) investment projects. In fact, that's what lots of people think a dividend check represents—what's left over after all the bills are paid and all investments undertaken. (My brother thinks this every time he picks up his dividend checks from his mailbox--yes he has them delivered to his home so he can caress them and smell them before depositing. He's weird.)

Therefore, under a residual dividend policy scheme, the distribution for any period will equal net income less the firm's target equity ratio, times its planned total capital spending program. The reason the target equity ratio is used is so that the dollars spent on the firm's planned capital spending program will be financed so as to maintain the firm's value-maximizing target capital structure.

The general equation for dividends under a residual policy is as follows:

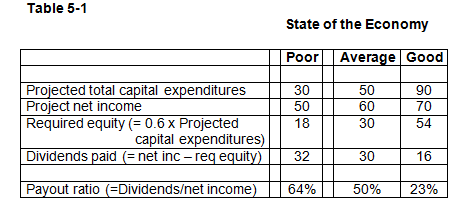

Table 5-1 applies some hypothetical pro forma numbers to Eqn 5-1 for Company X under various states of the economy. The numbers are in millions of dollars.

You can see that Company X's capital expenditures and net income are directly related to the health of the economy. This is plausible. Since the funds for capital expenditures are assumed to come from internally-generated sources (i.e., net income), then 60% of a dollar spent on new capital must come from net income (i.e., equity). This is shown in the third line of the Table. Subtracting the third line from the second line leaves the amount to be paid out as dividends under various states of the economy. The last line shows the payout ratio under different states of the economy and under different capital expenditure and net income amounts.

Instructor sidebar: Understand that the residual dividend policy assumes the firm's capital budgeting team has already done its homework in that they have already analyzed all positive NPV projects and determined the total dollar cost of this list of investments. Therefore, the next dollar spent on capital investment would have a $0 NPV and would be deemed unacceptable. (Recall our discussion of capital budgeting in Part 4 of the Money Flow lesson).

Residual policy and dividend volatility The residual dividend policy suggests that different investment spending plans will lead to different dividend levels and different dividend payout ratios. This table brings home a very important point about a residual-type policy—the policy leads to volatile dividends.

Two factors contribute to this volatility:

1. volatility in net income

2. varying investment opportunities

If the debt/equity ratio is maintained at its target percentage then (1) and (2) in combination mean a residual dividend policy will result in unstable dividends.

Now let's throw in some real-world facts. First, on an annual basis the reported net income of most firm's is far from constant. Second, the dollar expenditure necessary to exhaust all positive NPV projects for any planning period is far from stable. One period could be characterized by a flood of good projects whereas another period might be one with no or only a few good projects.

The unstable distributions that would result from strict adherence to the residual policy is precisely why firms do not follow it in practice. To do so would surely unleash negative signaling effects, a dividend by-product we discuss subsequently.

Some good things about the residual theory: Is there anything good we can say about the residual dividend model? Yes.

First, it forces the firm to simultaneously consider its target capital structure when raising capital for investment. Second, it forces the capital budgeting process to exhaust all positive NPV projects in arriving at its optimal investment spending plan. Third, the method reinforces the idea that earnings that can't be put to work in profitable projects should rightly be returned to shareholders as dividends (barring the negatives associated with signaling effects). Fourth, while firms should not use the residual model to set yearly dividend payouts, they can use the model to set the firm's long-run target payout ratio. For example, the data in Table 5-1 shows an average payout of about 46%. Firm X could use this payout percentage as a long-run payout benchmark over time. They might deviate from the benchmark on occasion but would return to it over the long haul.

Fifth, the residual idea can be easily combined with one of the various cash adjustment smoothing methods to be described below. In many cases this is how it is used in real-world dividend practice.

A similarity: Note the similarity between the MM dividend irrelevance theory and the residual theory: Under the residual model the only cash distributions that are made are ones that if used for investment would have a zero NPV, i.e., they can't be used to increase firm value. This feature of the model is quite similar to MM's dividend irrelevance idea discussed above—a dividend policy of distributing funds with a zero NPV cannot affect firm value—dividends distributed as a residual are irrelevant (excluding announcement effects).

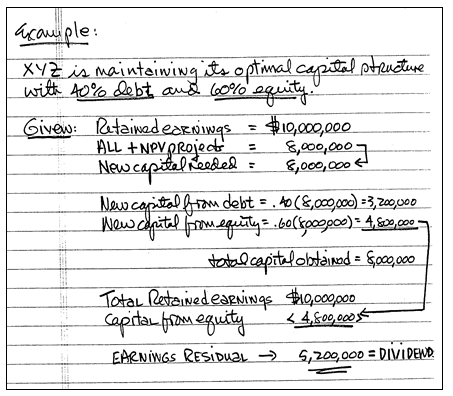

Let's work a problem: The XYZ Company is maintaining its target capital structure with 40 percent debt and 60 percent equity. Retained earnings this year is expected to be $10M. The capital budgeting staff has determined that all positive NPV projects for the coming planning period sum to $8M. The NPVs of projects beyond $8M in total spending equal zero.

Question: If the firm follows a strict residual dividend policy, determine what the dividends will be for the year?

Solution: The solution follows but don't look at it until you attempt to get the answer.

As you can see the residual model suggests that dividends will be $5.2M. The payout ratio in this case is 52 percent (= $5.2M/$10M), and the retention ratio is 48 percent = (1.00 - .52).

The bird-in-the-hand theory of dividends:

A by-product of the MM irrelevance argument is that stockholders are indifferent between dividends today and capital gains tomorrow. That is investors use the same discount rate in putting a present value on these two streams of cash flow even though these different streams are characterized by different risk levels.

The bird-in-the-hand theory of dividends takes a fundamentally different view of things. In particular, this theory holds that investors are not indifferent between dividends today and an equivalent amount of capital gains in the future. Rather they prefer a more certain dividend today to a more uncertain capital gain tomorrow.

What the bird-in-the-hand theory says is that investors discount the expected capital gain yield at a higher rate than the dividend yield. Thus, firms that engage in a high dividend payout (and thus have a low expected capital gain yield) can pay stockholders who prefer high current payout a lower total rate of return than firms that follow a low dividend payout. A lower required return results in a higher stock price for firms that match the high current payout pattern desired by bird-in-the-hand investors.

We can reference this idea by going back to Figure 5-1. where we trace out the dividends-today-versus-capital-gains-tomorrow tradeoff. Bird-in-the-hand investors would pay more for the stock of a firm that was positioned at point B than they would for an identical firm that was positioned at point A. Why? Because its cash flow stream is more certain.

The tax preference theory of dividends: The tax preference theory states that some investors prefer long-term capital gains to current dividend yield and will pay more for the stock of a firm that plows back its earnings into capital-appreciating projects instead of paying these earnings out as dividends. Taxes (and the time value of money) are the basis of this preference since stock price appreciation is taxed more favorably than dividend income.

While the Jobs and Growth Act of 2003 changed this result somewhat by reducing the tax rate on dividend income, the theory still has relevance due to the time value of money.

Let's explain the time value of money connection of the tax preference theory. The theory reflects the fact that nobody likes taxes. The time value of money relationship means a dollar of capital gain due at some point in the future will be taxed at a later date than a dollar of dividends paid today. This reduces the tax-adjusted cost of the capital gain below that of the dividend. In effect, investors that follow the tax-preference theory see the firm as a place their money can grow (temporarily) tax-free (your money can't be taxed if it's not paid out to you). This is not the case with dividends—when you receive a dividend you can't postpone the tax liability—the IRS is at your doorstep. "In this world nothing can be said to be certain, except death and taxes" - Benjamin Franklin.

The second reason supporting the tax preference idea is that once capital gains become an inter-generational transfer, the stock is re-priced by the IRS such that the capital gain is reduced to zero for recipients of the stock (this is called resetting the basis of the capital gain that is passed on to one's hairs—oops, I mean heirs). This results in zero tax. If investors are facing an inter-generational transfer they will tend to favor long-term capital gains and will oppose current dividend payments. The tax preference theory fits this situation.

Would the correct theory please stand up!

So which dividend theory is correct? First let's realize that the unrealistic assumptions surrounding MM's irrelevance theory take it out of contention—clearly real-world evidence suggests there is a relationship between a firm's stock price and its dividend policy. We cannot assume that investors are indifferent between dividend yield and capital gain yield, nor can we assume away the effects of brokerage fees and taxes. Simply put, financial markets are not "perfect," a condition upon which the irrelevance theory is predicated. However, as we explained, there is a real-world dividend behavior that results in dividend irrelevance. It's called the residual dividend model. So MM's irrelevance theory is not a total waste even with it's unrealistic assumptions.

Regarding the bird-in-the-hand and tax preference theories, it is empirically impossible to determine in the aggregate which policy will maximize the firm's stock price. This is because stock price is a function of many variables besides dividend payout. In any collection of firms you might assemble for study, it is statistically untenable to assume you can hold so many diverse variables constant such that the impact of dividend policy can be isolated. However, at the individual investor level these two theories have something to offer in terms of how stockholders behave. Some (younger) investors do consciously seek out stocks that have low payout and high expected capital gains; the tax preference theory would apply in this case. Some (retired) investors do value current income over uncertain capital gains; the bird-in-the-hand theory would explain their behavior. Let's also note that some mutual funds advertise based upon the capital appreciation or current income features of their portfolios.

"All models are wrong; some models are useful." George Box, statitician (1919 --)