Other Real-World Dividend Policies in Practice

A constant dividend payout strategy: Consider what is called a Constant Dividend Payout strategy. In this strategy the firm pre-specifies the annual dividend per share (DPS) at a fixed percent of annual earnings per share (EPS). That is

DPST = (fixed %) x EPST ,

where T represents a particular year. In this situation dividends will track earnings per share by a factor defined by the fixed percentage. That is

∆DPS/∆EPS = fixed %

This fixed percentage is set by management after taking into consideration such things as projected earnings growth, the needed retention rate from earnings necessary to carry out capital spending projects in the future, and other factors.

Given the perfect correlation between earnings and dividends, one problem with this policy is the potential instability of dividends. Negative earnings for a given year will force the dividend to be cancelled and the volatility of earnings and dividends will lead to unwanted signaling effects described above. For these and other reasons few firms follow this dividend strategy and it is not recommended.

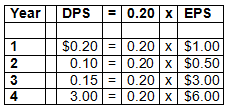

Example: Consider the pattern of DPS for the following three years if the ratio is set at a fixed 20% per year and EPS are as depicted in the last column of the table below.

Clearly the Constant Dividend Payout strategy leads to erratic dividends. Firms do not follow this strategy precisely because of the negative signaling effects that would be produced.

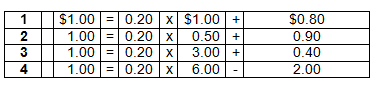

A discretionary constant payout policy: Firms can alter the constant payout strategy by adjusting the dollar dividend with discretionary cash additions to or subtractions from the dividend indicated by the constant payout policy. In this case the constant percentage payout is considered the target payout from which the firm can deviate as earnings change over time. Firms that follow this policy typically set the target payout percentage low so that even if earnings are poor one year, the fixed percentage floor will not have to be violated.

Example: Extending the previous table where management follows a fixed DPS equal to 20 percent of EPS as a target payout percentage, the firm is allowed the discretion to smooth annual dividends by adding or subtracting discretionary dollar amounts each period to the payout so as to maintain a constant DPS payout. In the table below the constant dollar DPS is $1.00. (Management has pre-specified that a long-term DPS of $1.00 is what can be maintained by the firm.)

This practice is demonstrated in the following table:

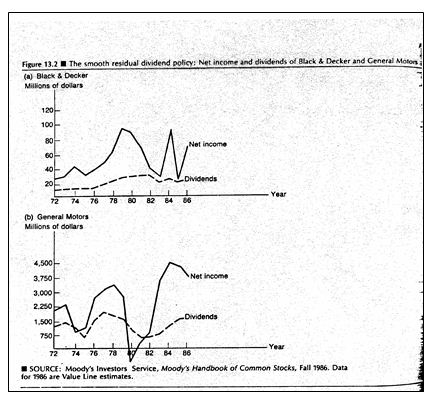

Notice that even though EPS experiences significant volatility over time, the policy is such that high earnings reduce temporarily high dividends and low earnings temporarily increase dividends resulting in a smoother payout than would be the case otherwise. While dividends are related to earnings, there is much less chance of signal mis-interpretation in such a case.This cash adjustment approach reasonably describes the previous time plot of dividends for Black and Decker and GM seen in Figure 5-2. (I do not know what the fixed payout target percentages were for these two companies).

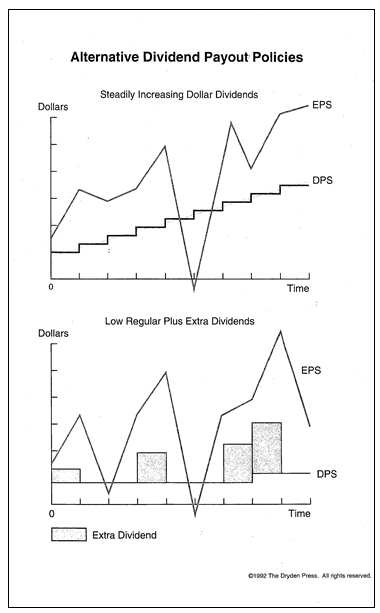

Additional dividend smoothing policies: The figure below presents two additional smoothing-type policies.The upper part of the figure shows dividends increasing at a steady pace in line with the long-run trend of earnings; short-run earnings volatility is overlooked in the payment of dividends. The reasoning here is that management expects the firm to be able maintain a growth rate of dividends equal to the longer-run trend growth in earnings.

The lower part of the figure shows what is called a low regular plus extra dividend policy. With this approach, dividends are purposely kept lower than justified by earnings growth as a routine matter. Extra cash is then paid out only when earnings are substantially higher than normal. As the Figure shows the minimal payout is adjusted upward only when management feels future earnings are certain enough so as to insure the new minimum can be maintained. As you can imagine, having to rescind a pre-announced increase in dividends that was thought to be permanent could result in a bunch of pink slips.

Figure 5-3: The two graphics follow: