The Financial Planning Process

While a full-fledged set of operating plans must outline plans in all areas of the business (e.g., marketing, processing and production, distribution, dividend policy, capital structure policy, overall working capital policy, employment and work force resources, risk management, etc.), in this final section, we will concentrate on one aspect of operating plans, that are concerned with financial planning and forecasting.

The long-term strategic financial plan: The firm's long-term (strategic) financial planning process takes from the general operating plan what financial resources will be needed in the future so as to achieve the firm's long-run objectives. Once integrated with the overall strategic plan it then outlines how these resources will be obtained. If future planned outcomes suggest more financial capital will be needed, a financial plan should uncover this fact and determine whether or not capital needs will come from internal or external sources. If external sources will be used, plans for tapping this capital in terms of both sources and amounts need to be formulated. Other considerations in a long-run strategic financial plan are the proposed acquisition of core fixed assets and other (related) businesses, the target capital structure, dividend policy, and the retirement of debt or the repurchase of stock.

Strategic financial plan forecasting and updating: The forecast horizon of the typical strategic financial plan can range from one to five years or more. Timely revision is part of the financial planning task. Usually firms in industries that are undergoing rapid change and operating uncertainty, say due to constant technological innovation, will have shorter planning horizons and will be required to update their forecasts more frequently. Firms in mature, stable industries can use longer planning horizons.

Some firms engage in what is called dynamic planning. A moving window planning horizon strategy is an example of dynamic planning. For example, a firm that follows a five-year horizon would drop the oldest year in the five-year window and add the most recent year and then revise the forecast accordingly. This would maintain a five-year horizon but its "rolling window" nature would be dynamic in that it would reflect changing market and economic conditions in a timely manner. In this case the five-year financial plan would always be as up-to-date as possible.

The short-run financial plan: The longer-run strategic financial plan does not usually meet the requirements for implementing timely operational guidance to management regarding the more immediate financing needs of the business. The short-run financial plan makes up for this shortcoming by breaking up the longer-run horizon into actionable short-run time intervals.The key input here is the one-to-five year sales forecast. A rolling sales forecast might also be used but can be cumbersome and mis-leading if the sales forecast is too closely correlated with the firm's core earning asset acquisitions or external funding requirements.

A typical one-year short-run financial plan is made up of the following six steps:

1. Determine the sales forecast for the coming year.

2. If the firm is operating at capacity, develop a quantitative idea of the additional core earning assets that will be needed to satisfy the sales forecast.

3. Using either a simple formulaic additional funds needed relationship or a more comprehensive pro forma income statement and balance sheet simulation, forecast the funds that will be needed to acquire core earning assets.

4. Compare the forecasted internally-generated funds with the total funds that will be needed. The difference between total funds needed and internally-generate funds constitutes the additional financial capital that will needed from external sources.

5. Given the external amount of funds needed, some plan of action should be spelled out about where these funds are to be obtained (e.g., short-term notes payable, long-term debt, the issuance of new stock, or some combination of all three sources).

6. Provide some type of feedback control loop such that unintended differences between funds needs and funds sources can be corrected.

The sales forecast: As mentioned above, the sales forecast is the most critical input in short-term financial planning models. The forecasting procedure typically starts with a historical review of past sales levels and growth rates along with internal data generated from the firm's sales staff, marketing, and perhaps a consulting service. External data can be used to see the correlations between the firm's sales and key macroeconomic data such as GDP, employment growth, and disposable personal income.

A pure historical data method may be used. For example, a one-year ahead sales forecast might look at the past five or ten years of sales figures for the company. From these data a growth rate of sales can be obtained using a simply time value of money formula. If management feels this growth rate is representative of the past and the coming year, it can be applied to the last year's sales level to provide a one-year-ahead forecast. Here's an example using a six-year historical time series of sales.

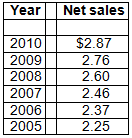

Example and a problem: The XYZ company's sales levels for the past six years (2005 – 2010) are provided in the table below (in millions of dollars).The sales figures are recorded at the end of the year:

Historical Sales Data for the XYZ Company

Required: Obtain the growth rate, g, of sales between 2005 and 2010 and compute the sales forecast for 2011.

Solution: Here we use the time value of money equation:

FVN = PV0 (1 + g)N .

Re-writing this equation in terms of our 2005 and 2010 sales we have:

FV2010 = PV2005 (1 + g)5 .

You can see that it is the reverse of the present value formula given in equation Eqn 3 for one year only. It asks the question, "What annually compounded growth rate, g, is necessary to make sales grow from $2.25 million at the end of 2005 to $2.87 million at the end of 2010?

FV2010 = the future value of sales in year 2010; PV2005 = the present value of sales in year 2005; g = the annual geometric growth of sales over the six-year time horizon; the exponent "5" provides for five compounding periods. Since sales are recorded at the end of the year there are only five years of compounding, not six.

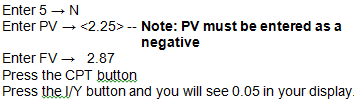

Using your Texas Instruments business calculator:

This means that over the past six years sales have been growing at an annually compounded rate of 5 percent.

Now, using the future value equation above we can write:

FV2011 = PV2010 (1 + 0.05)5

= $2.87 (1 + 0.05)5 .

Solving for FV2011 we get a sales forecast of $3.02 million for 2011.

Caution: A few caveats are in order when forecasting sales using the historical method:

1. Management is assuming the past is representative of the future. This might be true in a one-year setting. It typically will not be for longer forecasting horizons.

2. Using only six data points can give unreliable results if one-time sales highs or lows for either the beginning or end of the series occurs.

3. If management feels that the past growth rate is only partially representative of the future growth rate, intuitive adjustments can be imposed on the forecast.